Join me today in Mission Hills where I’ll be doing open house from 12-2pm!

2235 Linwood, #A4, San Diego (off Bandini)

2 br/2 ba, 832sf

YB: 1987

HOA fee = $425/mo.

LP = $699,900

Live in Mission Hills among the multi-million dollar homes and share similar ocean views! This cute and cozy 2br/2ba single-level home is at the top level of the Terraces of Mission Hills and is walking distance to the fabulous Old Town historic district including the Old Town Mexican Cafe! Get to Petco Park/downtown, Mission Beach, Hillcrest, or OB within minutes – you’ll love this location! Two primary suites, good-sized kitchen, fireplace, and your own washer and dryer inside. This gated community includes two assigned parking spaces too – wow! Close escrow in time for the big Fourth-of-July fireworks show!

How bad can it be in Mississippi? Oh wait, don’t answer that.

Median-priced homes in these states cost $300,000 or less, a significant discount compared with the U.S. median price of $402,343.

While these 14 states may have cheaper properties available, there are trade-offs to consider, like higher rates of poverty and fewer high-paying jobs compared with the rest of the country. Many of them are among the most rural in the United States, and incomes in rural areas tend to be lower than in urban cities.

In contrast, you’d need to make $197,057 to afford a median-priced home worth $739,200 in California — the highest amongst all states.

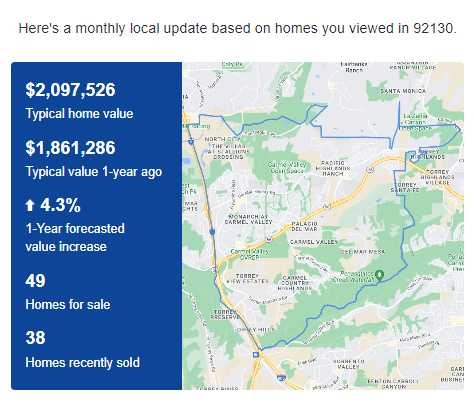

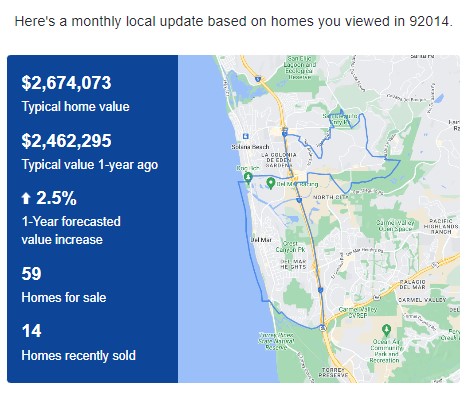

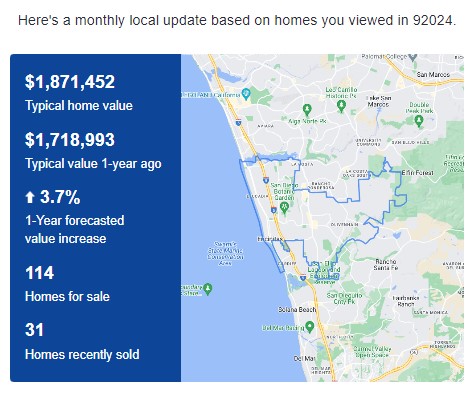

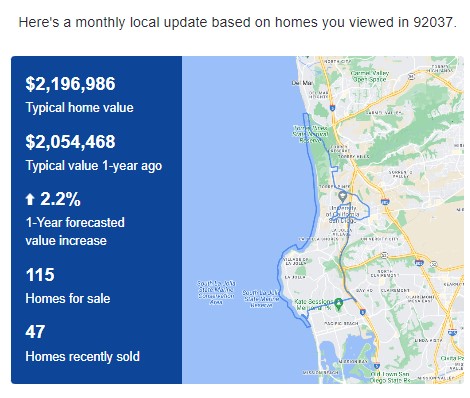

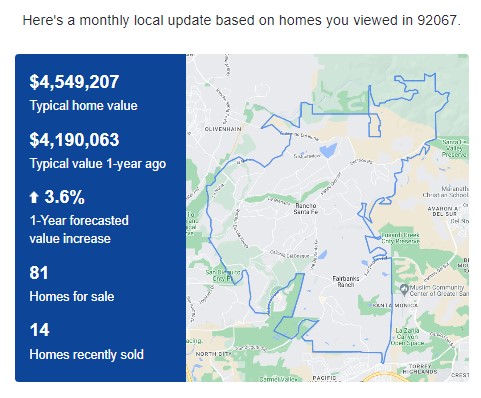

In February, their annual appreciation guesses were in the 3% to 4% range. In March, they got excited and bumped all local areas up to 4.9% to 6.3%! They are back to the 2.2%-3.9% range, with Carmel Valley clocking in with a solid 4.3% over the next 12 months.

It probably means that pricing will be fairly flat until next year:

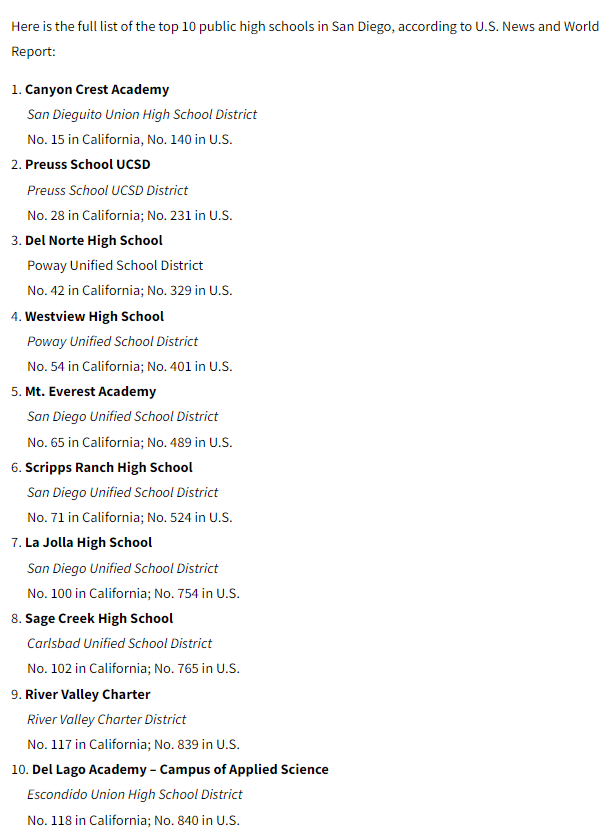

Carlsbad NW

Carlsbad SE Carlsbad NE Carmel Valley Del Mar Encinitas La Jolla Rancho Santa Fe

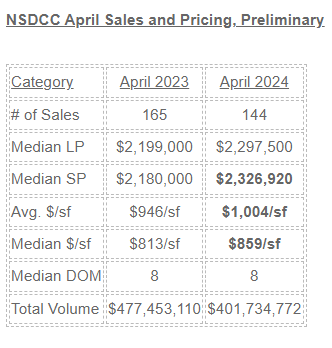

There may be a lot of turbulence around real estate these days, but sales keep happening!

The pricing metrics are up 5%-6% since last April, and we’re not done yet with sales this month. Helped by Easter being on March 31st this year, the final count of closings for April, 2024 is probably going to exceed last year’s 165 sales – wow!

It was so great to start the tour today with Pete’s new listing on the Encinitas Ranch Golf Course whose owners succumbed to the problem at hand. They get hit by golf balls, so provide a barrier and live with it.

This is way better than the alternative where potential buyers have to wonder about the impact. Know this – when a golf ball hits your roof, it sounds like a bomb went off.

We lost Gregg LeNoir Allman in 2017 at age 70, and we lost Dickie last week at age 80 – rest in peace. We won’t see anything like this again. (hat tip just some guy):

“Melissa” (sometimes called “Sweet Melissa”) is a song by American rock band the Allman Brothers Band, released in August 1972 as the second single from the group’s fourth album, Eat a Peach. The song was written by vocalist Gregg Allman in 1967, well before the founding of the group. Two demo versions from those years exist, including a version cut by the 31st of February, a band that featured Butch Trucks, the Allman Brothers’ later drummer. Allman sold the publishing rights later that year, but they were reacquired by manager Phil Walden in 1972.

The song’s title is frequently referred to incorrectly as “Sweet Melissa” due to the lyric being sung at the end of each of the first two choruses.

The version on Eat a Peach was recorded in tribute to Duane Allman, who considered the song among his brother’s best and a personal favorite. He died in a motorcycle accident six weeks before its most famous rendition was recorded.

Gregg Allman penned the song in late 1967. He had previously struggled to create any songs with substance, and “Melissa” was among the first that survived after nearly 300 attempts to write a song he deemed good enough. Staying at the Evergreen Motel in Pensacola, Florida, he picked up Duane’s guitar which was tuned to open E and immediately felt inspired by the natural tuning. Words came naturally, but he stumbled on the name of the love interest. The song’s namesake was almost settled as Delilah before Melissa came to Allman at a grocery store where he was buying milk late one night, as he told the story in his memoir, My Cross to Bear:

It was my turn to get the coffee and juice for everyone, and I went to this twenty-four-hour grocery store, one of the few in town. There were two people at the cash registers, but only one other customer besides myself. She was an older Spanish lady, wearing the colorful shawls, with her hair all stacked up on her head. And she had what seemed to be her granddaughter with her, who was at the age when kids discover they have legs that will run. She was jumping and dancing; she looked like a little puppet. I went around getting my stuff, and at one point she was the next aisle over, and I heard her little feet run all the way down the aisle. And the woman said, “No, wait, Melissa. Come back—don’t run away, Melissa!” I went, “Sweet Melissa.” I could’ve gone over there and kissed that woman. As a matter of fact, we came down and met each other at the end of the aisle, and I looked at her and said, “Thank you so much.” She probably went straight home and said, “I met a crazy man at the fucking grocery.”

Allman rushed home and incorporated the name into the partially completed song, later introducing it to his brother: “[I] played it for my brother and he said, ‘It’s pretty good—for a love song. It ain’t rock and roll that makes me move my ass.’ He could be tough that way.” The duo produced a demo recording of “Melissa” that later surfaced on One More Try, a compilation of outtakes released thirty years later. In 1968, the duo recorded it during a demo session with the 31st of February, a band that featured Butch Trucks, the Allman Brothers’ later drummer. That version is thought to have featured the debut recorded slide guitar performance from Duane Allman, and the entire session was later compiled into Duane & Greg Allman, released in 1972. Gregg Allman sold the publishing rights to “Melissa”, as well “God Rest His Soul” (a tribute to Martin Luther King Jr.), to producer Steve Alaimo for $250 (equivalent to $2,190 in 2023) shortly thereafter. He had been tied up in Los Angeles, contractually bound by Liberty Records (who had previously issued albums by the Allmans’ first band, the Hour Glass), and used the money to buy an airplane ticket to fly back.

When Duane Allman was killed in a motorcycle accident in 1971, his brother performed the song at his funeral, as he had grown to like the song over the years. Gregg Allman commented that it “didn’t sit right” that he used one of his brother’s old guitars for the performance, but he nonetheless got through it; he called it “my brother’s favorite song that I ever wrote.” Both because he did not own the rights and found it “too soft” for the band’s repertoire, he never mentioned the song to the members of the Allman Brothers Band. Following Duane’s death, manager Phil Walden arranged to buy back the publishing rights in order to record the song for Eat a Peach, the band’s fourth album. Gregg brought it to the studio the day following his birthday and the band recorded it that afternoon at Criteria Studios in Miami, Florida. They felt it lacked a compelling instrumental backing element so guitarist Dickey Betts created the song’s lead guitar line.

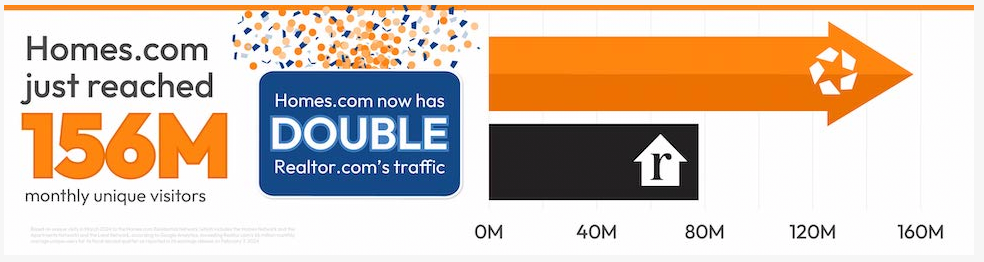

They are only three months into their mega-launch of Homes.com, and CoStar founder and president Andy Florance is already taking victory laps. He is also the #1 cheerleader for buyers going directly to the listing agent, which will be the end result of all the changes underway. Here’s Andy talking in front of a group of realtors:

Florance said Homes.com’s “Your Listing, Your Lead” model was the antidote to agent and consumer frustrations, as evidenced by triple-digit traffic growth during Q3 2023 that gave them a contested lead on Realtor.com as the second-most-trafficked residential portal.

“In the rest of the world, when an agent has a listing, their name is on the listing, their phone number is on the listing, and there’s branding happening,” he said to riotous applause. “Only in the United States is it the portals’ brand goes on the listing rather than the agents’ brand. That’s bizarre.”

Although CoStar didn’t reveal its exact plans for Matterport, Florance did outline a plan to capitalize on digital twinning, a term used to describe hyper-realistic 3D listing experiences.

Florance said digital twinning could enable homebuyers to visualize what their current home furnishings would look like in a new home, play with renovation options for a fixer-upper, or walk with a virtual agent through a virtual listing.

“In residential focus groups, homebuyers are telling us that they prefer listings that offer 3D digital twins so that they can best understand the property,” he said. “Adding virtual reality to Matterport, you can take a virtual tour of the property with your virtual agent who will walk into the space with you.

Florance spent a few moments of the call focusing on buyer-broker commissions and reiterated Homes.com’s potential value when NAR’s settlement terms go into effect this summer. Florance said Homes.com will give buyers an avenue to directly connect with listing agents to view a home, bypassing the potential pressure to sign a representation agreement before they’re ready.

“Currently only 30 percent of buyer agents ever get a written agreement at any point in the transaction process,” he said. “Homes.com connects homebuyers directly with the listing agent, so they can arrange to see the house with no paperwork or commitments.”

“We are increasingly confident in our ability to build out the number one residential marketplace in terms of traffic revenue and profitability in the years ahead,” he added.

CoStar owns LoopNet, the website for commerical listings, as well asten-x.com/which is an online auction house for commercial properties. It won’t be long before they bring auctions to the residential market, will it?

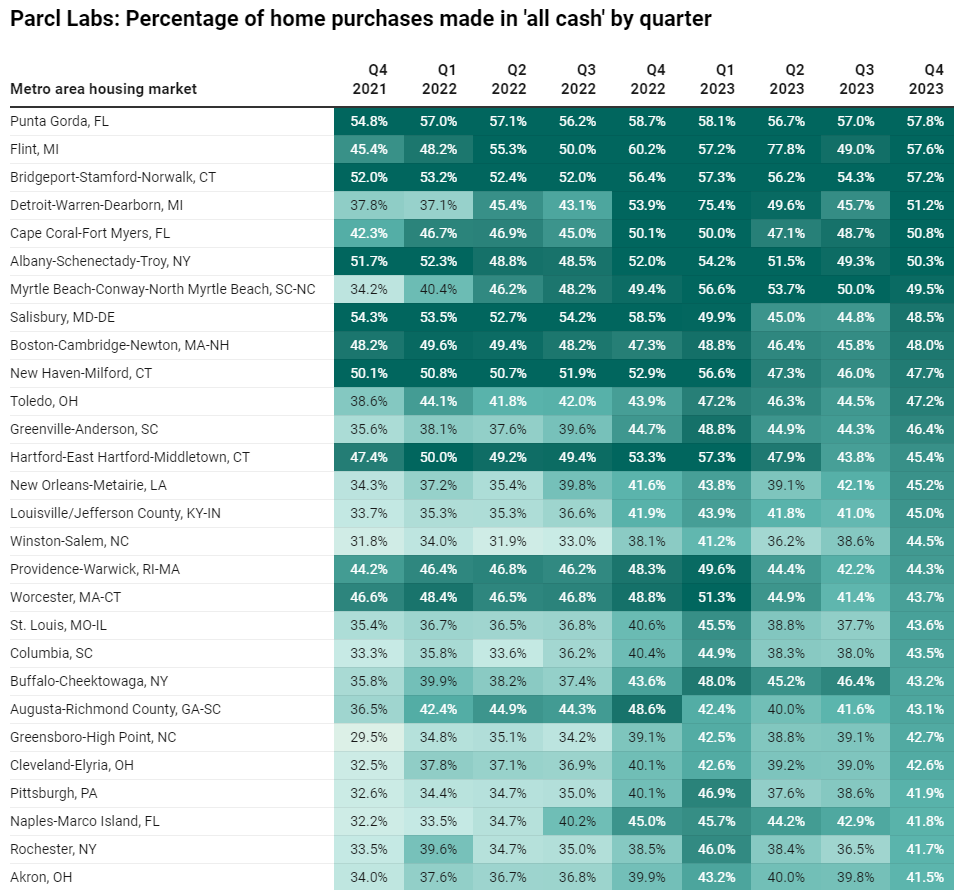

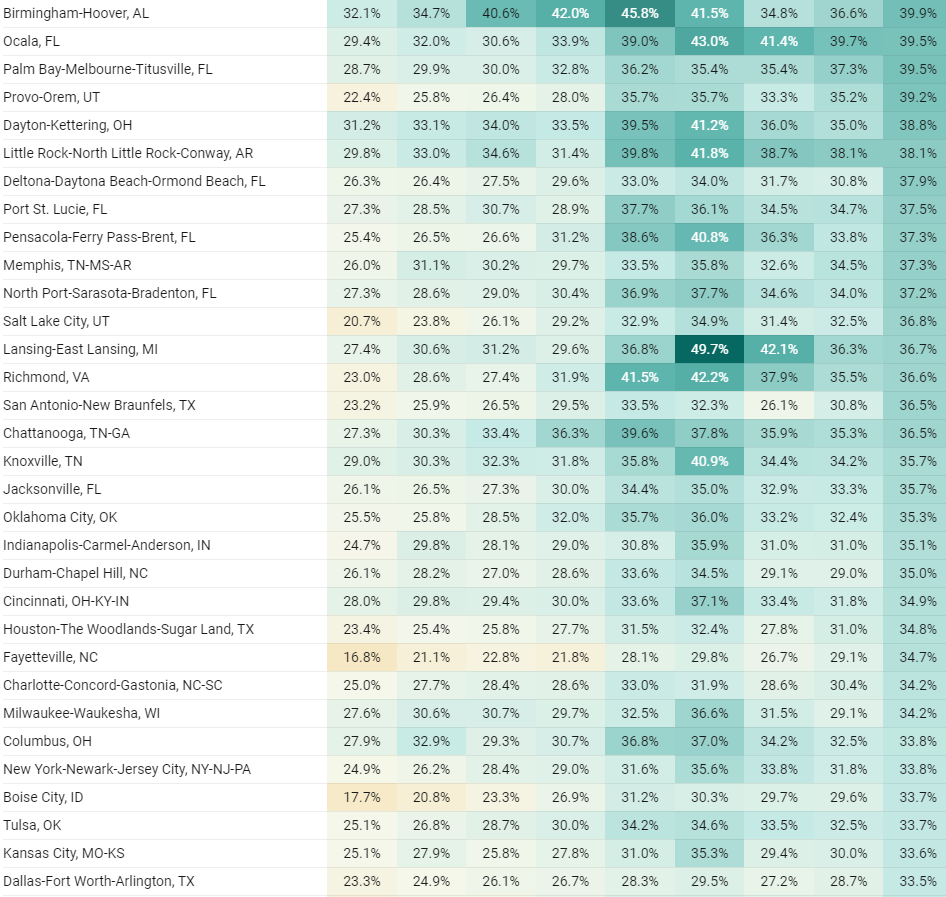

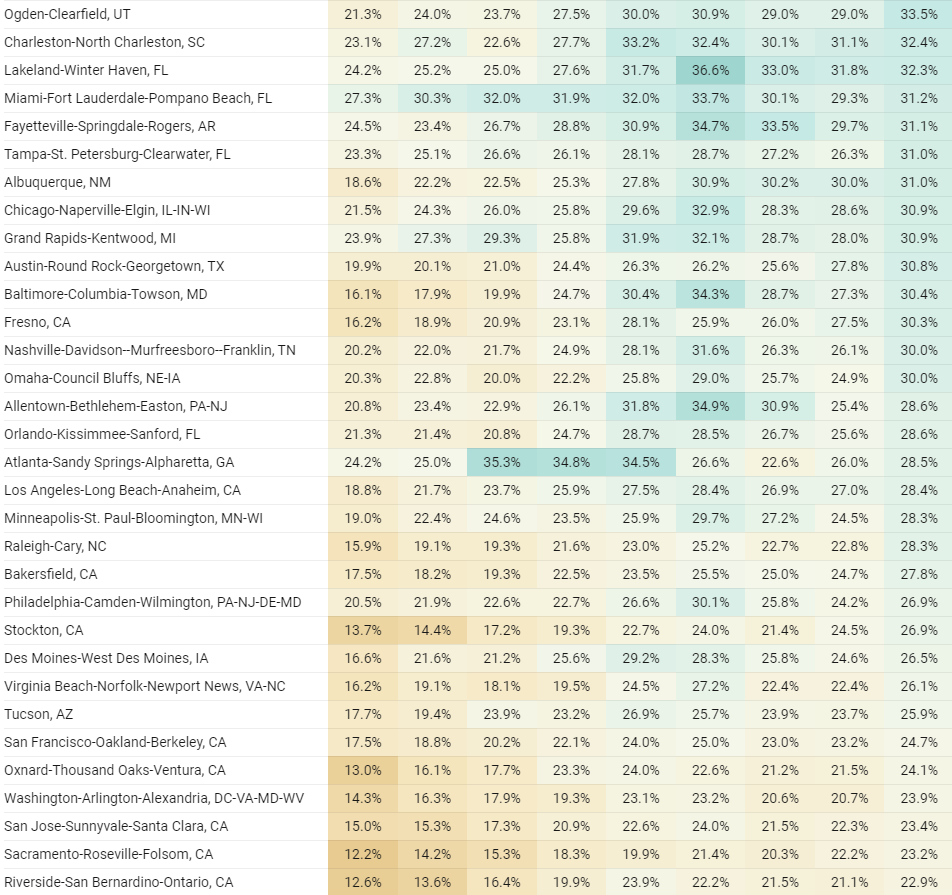

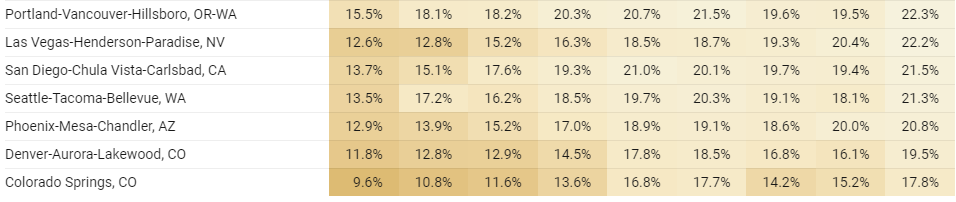

The locked-in effect has been bandied about for the last couple of years as the reason why the inventory remains thin. But it’s not stopping those who want to pay cash and avoid a mortgage altogether – every area is showing increases in the all-cash purchases.

If you don’t want to leave your local neighborhood, then yes, you’re locked in – the higher prices and rates make it prohibitive to move. But for the homeowners who don’t mind leaving town, they can take their winnings and pay cash for their next house!

Don’t let higher rates stop you. Thirty-eight percent of the homes in America are paid in full – join the club!