As we roll into the Lowball Season, we’re reminded of what happened in Carmel Valley at the end of 2022. Everyone’s home equity was built up fast and easy over the last 3.5 years, and the more desperate sellers might give it back in big chunks if they had to….and with 8% mortgage rates, they might have to.

How did it turn out last year?

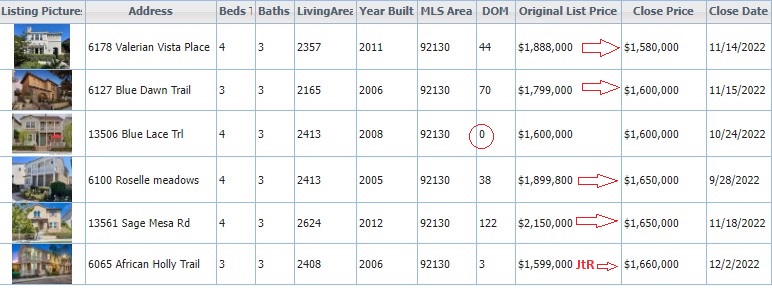

The fourth quarter of 2022 was brutal for the entry-level homes in Pacific Highlands Ranch:

The list pricing was fairly optimistic, and after 30+ days on the market, the lowballers came out. By the time my listing hit the market (the last on the list), our list price was revised down to $1,599,000 to ensure we would sell right away – and hopefully for more, which we did, and stop the trend.

Did the pricing bounce back this year?

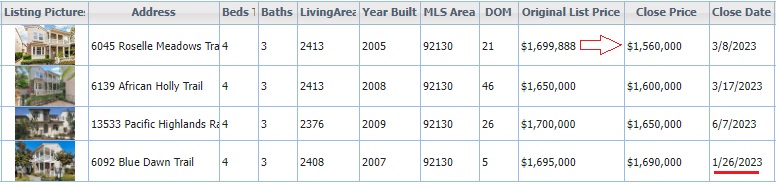

The first sale of 2023 closed right away for $1,690,000, and it seemed like the comeback was underway. But then the next sale was $1,560,000 – and it has hampered the pricing ever since:

The big threat isn’t going to be foreclosures. It will be the equity-rich sellers who dump on price to get out – and they will impact future sales. A couple of lowballs can turn into a trend!

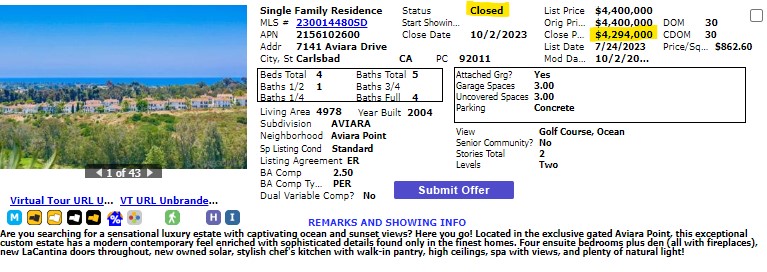

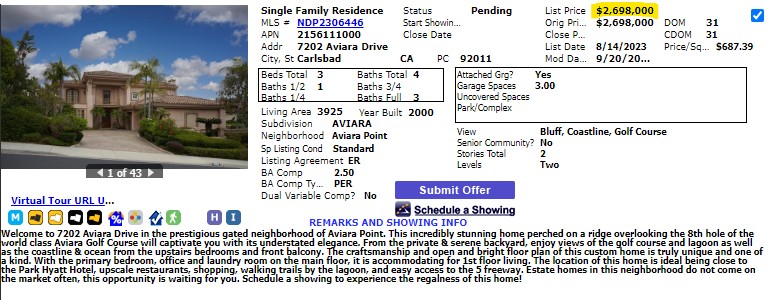

Our listing on Aviara Drive closed escrow yesterday, setting a new record for highest price ever in Aviara (an area of 2,025 homes in SW Carlsbad). It was one of those sales that needed everything to go right, because we were thrown a real knuckleball right in the middle.

A couple of weeks into our listing period, I got a phone call from a fellow Compass agent. She had just listed a home across the street on behalf of out-of-town owners who weren’t using the home enough to justify keeping it. She was wondering about the activity on my listing, and I told her we had quite a few showings and a lower cash offer.

My next question was obvious – what is your price?

“They want to blow it out, so we listed for $2,698,000”.

The price gap between us was Grand Canyon-esque!

Thankfully, the real estate gods are looking down favorably on me. Out-of-country cash buyers looking for a second home descended upon her listing first, because let’s face it – it looked like a bargain. They made an offer to purchase it, but for some reason “it didn’t come together”.

Instead, they came over to my listing and paid $4,294,000 to get the ocean view. They plan to invest another $1,000,000+ to make it exactly what they want.

Two other fortuitous things happened.

A. Their agent was a past client of ours! She had purchased a home with us early in the covid days, and has since got her license and become an agent. She knew she could count on us to help make the deal.

B. At the first showing, I casually mentioned to the buyers that the Chilean burglary gangs have been active throughout Southern California, and there were a couple of cases in this neighborhood. He shrugged it off and said, “We’re from Mexico City!”

Did we have to spend the $80,000 in repairs and improvements? Absolutely, and it’s what brought us to a neutral space so buyers could easily see what they could do with it. Everyone will put their own touches on a home, but they neeed a neutral palatte to start with!

For a bonus, we did a photography shoot of the team at the house before it was over:

I’m a lucky guy!

(Not pictured is Natalie Klinge who was on tour. We need to photoshop her in!)

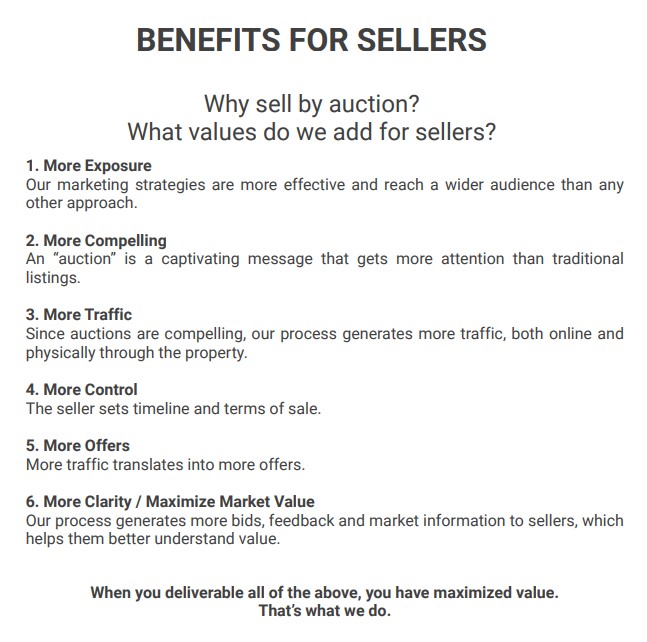

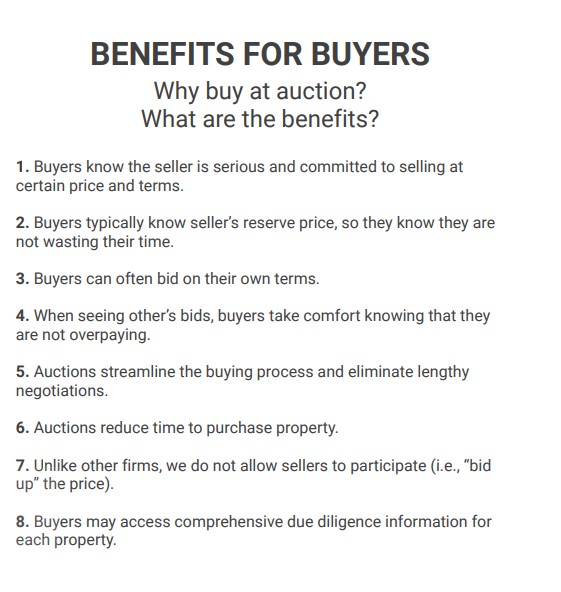

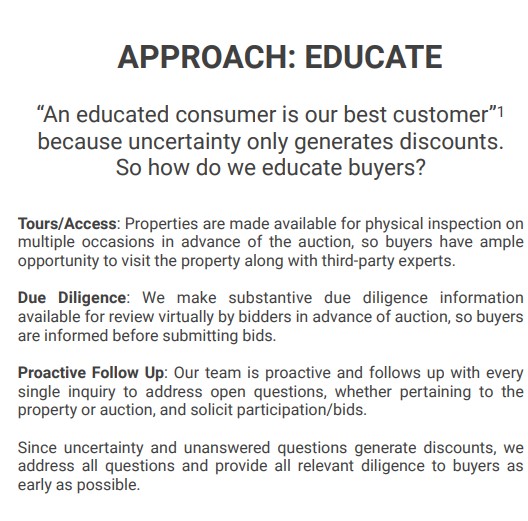

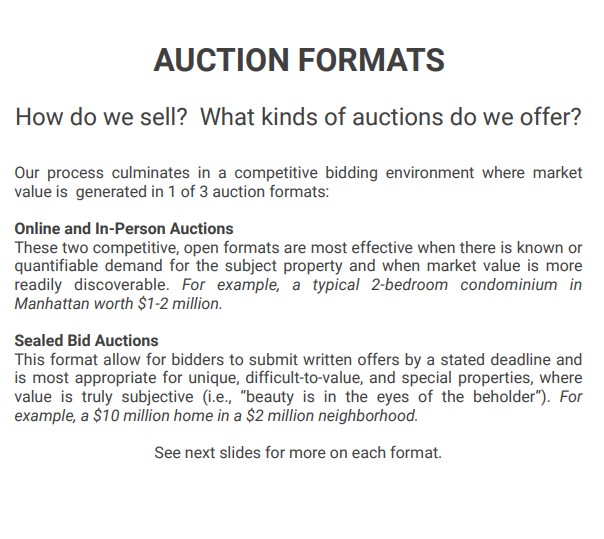

I’ve pitched Robert Reffkin a couple of times about auctions. Even though he is the Compass CEO and running an operation of 30,000 agents and employees, he replies to every email!

He said they are working on the things that agents ask about the most. Apparently, he’s getting more inquiries because Compass has partnered with Paramount Realty USA, a national auction house!

I doubt I’ll be using their service, but it is fantastic to see autions becoming more mainstream. Hopefully they will be the primary way we sell homes some day. They wash out all the agent shenanigans and deliver the pure and most transparent way to sell a home.

Here are slides from their pitch:

Having buyers complete their home inspections prior to the auction would eliminate most of the problems we encounter now during escrow. Currently, the contingency of home inspection can screw up a sale in two different ways. 1) Buyers find unknown surprises and use them to their advantage to work over the sellers (again), and 2) Buyers aren’t as committed to closing the deal because they know they have contingencies that give them the ability to walk away, no charge. Auctions would wipe out all of the above.

But my favorite thing about the auction format is that it gives everyone a fair shot at buying the home, which isn’t guaranteed today…unless you list your home with me. I received four offers on my latest listing, and we have a winner:

By the end of last year, the active-listing count was down to 288, so there should be a steady decline over the next three months – with more sellers cancelling their listing than selling.

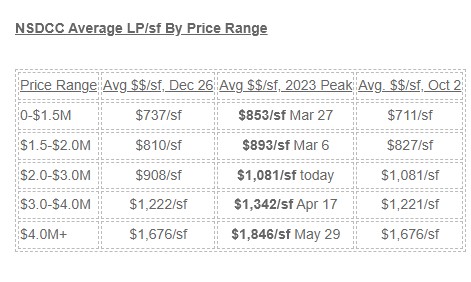

The pricing ride through 2023 has been bumpy – and the similarities today to the beginning of the year are very interesting. On the high-end, the average list-pricing is back to where we started.

I have mentioned repeatedly that the buyer-agent is a dead man walking. All forces within the industry are combining to push the buyer-agent out of the equation, and home buyers will be worse off because they will only have faux representation when buying directly from the listing agents.

Everything is negotiable……well, except the buyer-agent commission. From the Code of Ethics:

The Code of Ethics Standard of Practice 16-16 prohibits buyer-brokers from “using the terms of an offer to purchase to attempt to modify the listing broker’s offer of compensation.” Thus, the buyer-broker cannot attempt to condition the purchase of a home on the seller-broker’s agreement to adjust the amount of compensation offered to the buyer-broker.

Second, the Code of Ethics’s Standard of Practice 3-2 requires that any modification in the compensation offered to the buyer-broker “must be communicated to the [buyer-broker] prior to the time that [buyer-broker] submits an offer to purchase the property. And once a buyer-broker “has submitted an offer to purchase the property, the listing broker may not attempt to unilaterally modify the offered compensation.”

Third, Case Interpretation #16-15 advises that any negotiations regarding the buyer-broker’s commission “should be completed prior to the showing of the property.”

The buyer-agent is NOT allowed to negotiate their commission during the offer process!

What’s worse is that any negotiation of the commission must happen BEFORE the home is shown to the buyer. How many listing agents will agree to pay more commission before the buyer sees the home? The answer is zero.

The pending lawsuits against realtors are all about the seller being required to pay the buyer-agent’s commission. Miraculously, ReMax and Anywhere have already settled, and the whole thing could get resolved shortly. But it has been univeral among observers that the end result will be that home sellers will not be required to pay ANY commission to the buyer-agents. It will be optional instead.

Two things will happen:

The buyer-agents will be even more likely to steer their clients to where they can get a commission.

There will be even more shenanigans by listing agents.

Rob lays it out here, starting around the 26-minute mark:

It means that the buyer-agents will have to either live with the commission that the seller is offering (if any) and steer their buyers to those homes, or have an agreement with their buyer to be paid directly by them. While that sounds nice, it is a complete change to the business and most agents won’t be able to justify being paid for their services. When buyers can just go direct to the listing agent for free – which the listing agents will be advertising – they will be very reluctant to be contractually obligated to pay a buyer-agent.

Now that summer is over and mortgage rates are screaming towards 8%, many will assume that the real estate market has gone dormant for the rest of the year.

But my strategy of effectively sprucing up the house and utlizing an attractive price keeps working. Towards the end of this video I show the recent comps for the neighborhood, and you’ll see that ‘attractive’ factors in the time of year and market conditions but isn’t under market – especially considering that the home has the original roof, original windows & doors, and original bathrooms:

Forbes screened more than 800 locales in the U.S. for everything from climate change risk to crime to availability of doctors. We then compared those that made the cut for what they offered in leisure pursuits—from the arts, fine dining and learning to hiking, skiing, watersports and golf.

The local real estate market between La Jolla and Carlsbad has been fairly healthy lately, and feels in better shape than it did last year at this time when we were still getting over the initial shock or higher rates.

How will the rest of this year turn out?

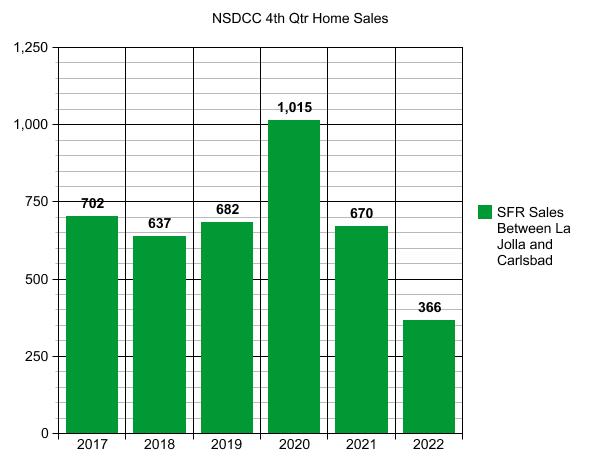

The recent burst that pushed up mortgage rates – now near 8% – will cause most people to sit out the rest of the year. Heck, it’s the holidays! Sales in the fourth quarter of 2023 will plunge and probably set the all-time low. I’m hoping we have 300 sales!

Want to know the history?

In 2007, we had 460 closings in the fourth quarter, and in 2008 we had 461 closings. By 2009 the market was already on the upswing, and there were 671 4Q houses sold between La Jolla and Carlsbad.

Last year, we saw some successful fourth-quarter lowballing where sellers dumped 10% or more on price to get out, and we’ll see more this year! But only for those buyers and agents who cause it to happen.

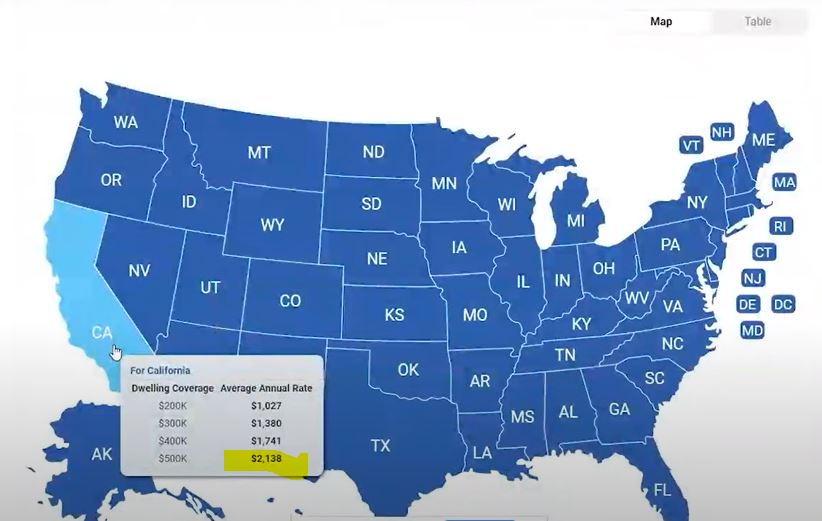

Currently buyers are having to pay 2x or 3x the previous bill for homeowners insurance, due to the lack of options because the big insurance companies have stopped writing policies in California. Some are blaming climate change, and guys like Carl Demaio are blaming Biden, but with a little digging it looks like the insurance-companies requests to raise premiums have been stalled for years. California’s average home insurance rate is $1,225 per year for $250,000 in dwelling coverage is about 14% lower than the US average, according to Bankrate. The thought of insurance premiums being 30% higher sure sounds better than 2x or 3x!

Full story from the LAT:

After a summer that saw many of California’s top home insurers pull back from the state market, Insurance Commissioner Ricardo Lara announced Thursday that he struck a deal with the insurance industry to encourage new coverage in the state.

Insurers, Lara said, agreed to return to the high-risk fire zones in the state in exchange for a number of concessions that will make it easier, in theory, for them to get higher rate increases through the state regulator more quickly. The announcement comes the week after negotiations in Sacramento over a legislative response to the home insurance market fell apart.

Gov. Gavin Newsom also issued an executive order on Thursday afternoon commanding the insurance commissioner to “take prompt regulatory action to strengthen and stabilize California’s marketplace” and consider whether emergency action could be necessary.

The changes are slated to go into effect by the end of 2024, but the hope is that insurers will return to writing new homeowners policies in California sooner. Leading insurers such as State Farm, USAA and Allstate all have requests for rate increases pending with the state insurance department, and are requesting hikes of 28.1 percent, 30.6 percent and 39.6 percent, respectively.

If approved, each company would be allowed to raise its total premiums in the state by that amount, but the rate increase can be distributed differently among homeowners: a cabin in the woods might see a 200 percent jump while a home in San Francisco could see little to no change.

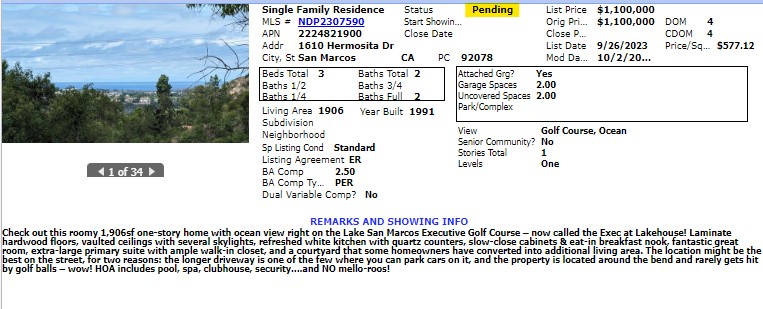

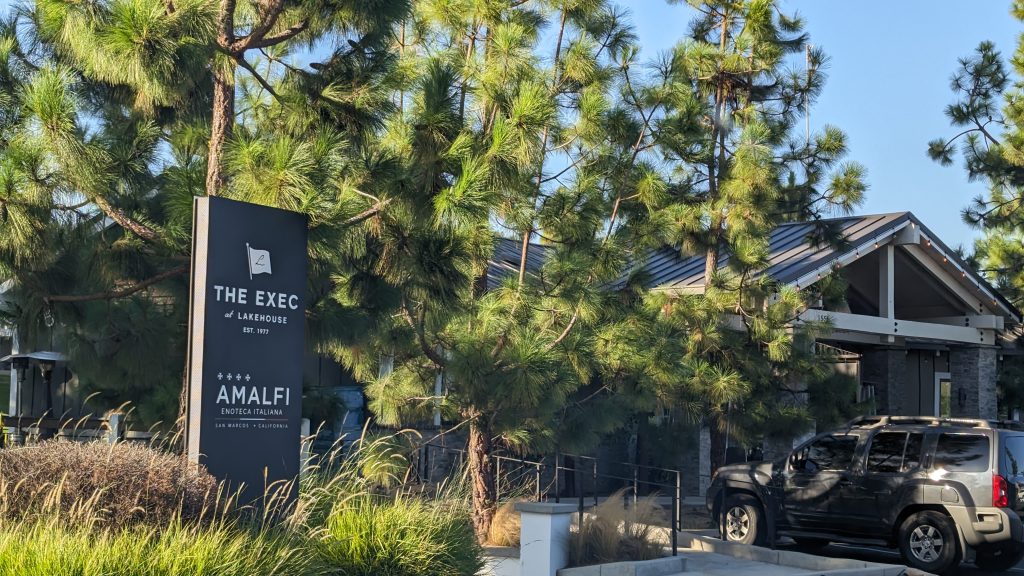

Check out our new listing of a roomy 1,906sf one-story home right on the Lake San Marcos Executive Golf Course – now called the Exec at Lakehouse! Hardwood floors, vaulted ceilings with several skylights, refreshed white kitchen with quartz counters & eat-in breakfast nook, fantastic great room, extra-large primary suite with ample walk-in closet, and a courtyard that some homeowners have converted into additional living area. The location might be the best on the street, for two reasons: the longer driveway is one of the few where you can park cars on it, and the property is around the bend and rarely gets hit by golf balls – wow!

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.