The was the Inventory Watch report in mid-December last year:

Today’s report:

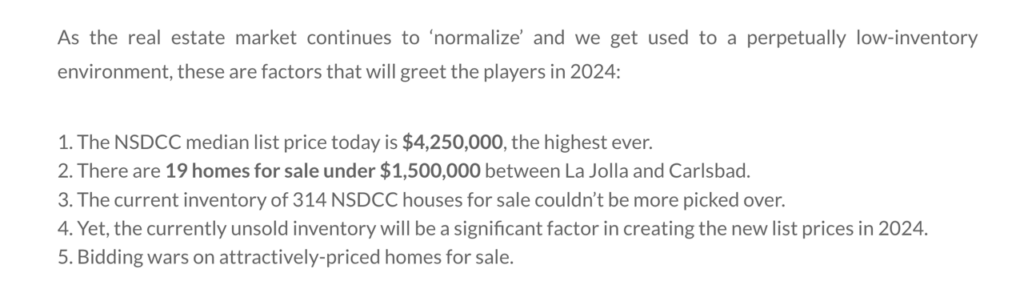

The NSDCC median list price today is $3,895,000. (It was higher than $4M until April 15th this year).

There are 22 houses for sale priced under $1,500,000 between La Jolla and Carlsbad.

The current inventory is 386 NSDCC active listings (+23% YoY) that are also very picked over.

There are 185 actives priced over $4,000,000, and their average list price is $11,164,026.

At this point, most everyone is in the wait-and-see mode for 2025, but I think I have another sale in me this year. Donna is feverishly preparing five homes for sale that will hit the open market in January and February. Instead of some holiday relaxing with family, we are in full-tilt boogie mode and pedaling as fast as we can – let’s go 2025!

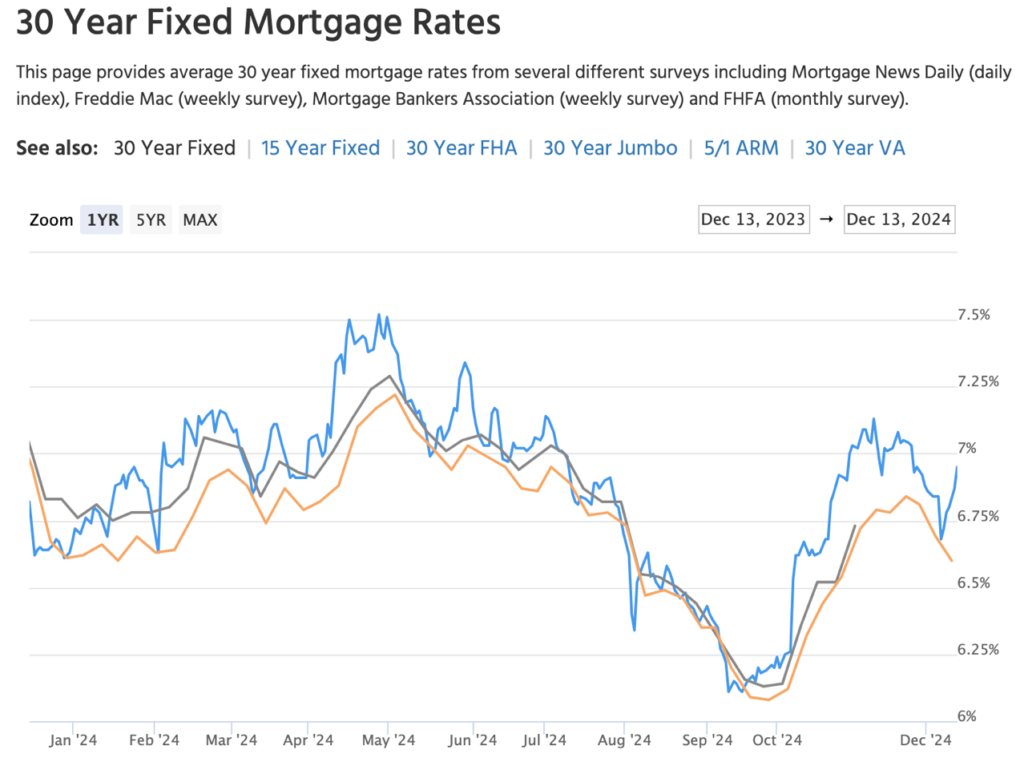

Rates are in the spotlight again as 2025 approaches. That short-lived dip to two-year lows prompted renewed optimism for home buyers and bumped sales volume, then the rebound in October brought a reminder of unpredictability. Rates are likely to remain volatile throughout next year, say Zillow economists.

Read on for more about rates and four more predictions for 2025.

Housing market activity will pick up, home value growth will cool

“Buying a home in 2024 was surprisingly competitive given how high the affordability hurdle became,” says Zillow Chief Economist Skylar Olsen. “More inventory should shake loose in 2025, giving buyers a bit more room to breathe.”

Expect to see more sales and only a modest 2.6% increase in home value growth in 2025, as the market slowly becomes unstuck. This is mainly because we expect more sellers to list next year. A steadier market could make for simpler pricing conversations with those seller clients.

Some markets are expected to outperform this forecast, such as Hartford, Connecticut (4.2% home value growth), Providence, Rhode Island (3.9% growth), and Miami (3.8% growth).

But markets like New Orleans (-3.8%) and San Francisco (-2.3%) are expected to see declines, while Austin is predicted to have minimal growth (0.4%).

Mortgage rates will remain volatile

Borrowing costs should ease in 2025, but as we saw in 2024, mortgage rates rarely do what’s expected of them. What’s more certain is that buyers should expect plenty of ups and downs throughout the year. Also expect sprints of refinancing — which can present conversation opportunities of their own — during the rate dips.

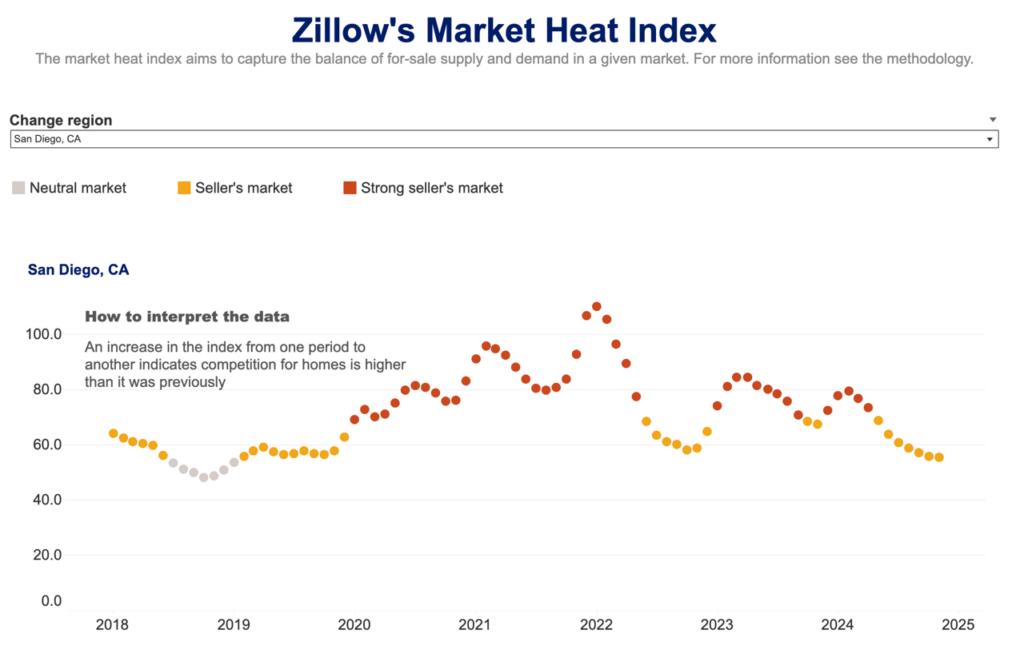

Buyer’s markets will spread to the Southwest

As of November 2024, a total of 25 major metro areas, mostly in the South and Southeast, were considered buyers markets, according toZillow’s Market Heat Index. Zillow predicts buyers markets will spread to the Southwest in 2025 as inventory continues to come unstuck in relatively affordable markets.

These buyers markets should see the greatest number of movers, while sellers will feel the heat of competition. But if mortgage rates fall more than expected, it dims the prospect that buyers markets will spread west. A significant mortgage rate dip would bring more buyers back to the market, again tilting negotiating power in favor of sellers.

More Americans will embrace small-home living

The pandemic-era need for more space is coming to an end. In 2025, buyers will increasingly embrace smaller homes as a more sustainable and affordable way to live.

The word “cozy” is appearing in more listings — 35% more in 2024 compared to 2023 — reflecting design trends that have shifted away from spacious open floor plans, toward more contained spaces that save both builders and buyers money.

John is talking about builders here but I couldn’t pass up his mention of last January and February being sensational, and then fizzling out. If rates start climbing again (and it was a bad week – see above), we could have a surge of new listings colliding with rising rates that together really scare off the buyers.

First, a look back

After more than a few rough spots in 2023, January and February of this year were nothing short of sensational. But that soon fizzled as mortgage rates regained their unwelcome upward momentum and sapped much of the wind out of the sails of the spring selling season. As Dillan said, “Once we got into those core spring selling season months—March, April, May—rates went up to 7%–7.5%,” and momentum slowed.

Part of this is the return of normal seasonality to the housing market. Cara highlighted this: “Seasonality has returned, and people have to accept that.” She noted that builders are learning to navigate a market where traditional patterns are re-emerging post-Covid, offering some stability amid uncertainty.

But that beginning-of-the-year head fake has possibly colored how we view the year. The housing market took every punch high rates had to offer yet was still standing by year’s end. That many see 2024 as a disappointment, then, seems unfair. Maybe LeBron cooled off after a monster first quarter, but he still wound up with a solid 25 points. (That’s two sports analogies in one bullet. Nice.)

Some things change, some things don’t

Though the Sunbelt and more affordable markets remain the growth loci, high-flying states like Florida and Texas have seen setbacks. Rising listings and new home inventory have softened sales in many markets in those states, even while other parts of the Southeast continue to thrive.

One thing that has not changed is the continuing dominance of larger builders. Jody called the growing market share of public builders—nearly half of all new home sales— “mind-boggling” (obviously, she hasn’t seen Blades of Glory). Access to capital and land, the ability to negotiate national contracts, and integrated information systems give bigger builders an edge.

Smaller private builders, though, are still in the game. They can carve out a niche with their local knowledge, long-term relationships, nimbleness in going after land, and sometimes partnering with bigger players. As Jody explained, “Private builders are often very well-connected locally.…They dominate specialty sites, like close-in transit-oriented locations, that public builders shy away from.”

If it is changing at all, affordability is another item that is trending for the worse. Home sales to first-time buyers are at record lows while rising prices and still-high mortgage rates don’t offer much hope for improvement. Affordability is something we are all keeping an eye on.

Not sure if you noticed, but we had an election

While there are some potential pluses with a new administration, like regulatory relief that could lower building costs or a friendlier development environment, uncertainties are looming over 2025. A couple of those stand out:

Threatened tariffs against Mexico, Canada, and China have the potential to reinflame inflation. High inflation means higher rates, which worsens affordability and makes builder buydowns more expensive—and more necessary.

Immigration restrictions would likely exacerbate labor shortages and raise labor costs. They could also deplete demand, particularly if there are restrictions on the H1B visas that many high-earning tech sector workers rely upon.

Though builders face these uncertainties, they have proven adept at figuring out ways to find buyers. With buydowns, more speculatively built homes to maintain absorption levels, and tapping into resale broker networks, builders have found ways to succeed. Success breeds optimism, and most builders forecast sustained growth for 2025.

For more and more people nearing or entering retirement, the South continues to be a draw, from Hot Springs, Arkansas, to Vero Beach, Florida, and plenty of zip codes in between. More American families have moved to this region than any other part of the country for the past decade, and that trend is expected to continue.

To identify the South’s best places to retire for 2024, Investopedia, a financial news and education website where I serve as Editor-in-Chief, partnered with Southern Living for the second year. We evaluated economic and livability metrics using data on housing prices, median income levels, and proximity to recreation and cultural activities, among other criteria. We interviewed locals, depended on the experience of Southern Living editors, and looked for spots where the quality of life is high.

Although our list contains just 10 locations, we know that there are many others in the region that warrant a mention. But when it comes to affordability and getting your money’s worth in retirement, this group gives you a great place to start. – Caleb Silver, Editor-in-Chief, Investopedia

Last Friday I had my nine reasons why inventory is going to surge in 2025, and it’s going to start up in January just like it did this year. It wasn’t a bad thing in 2024 because NSDCC sales have increased +6% year-over-year as the demand picked up some of the extra supply.

But as we saw in August, the demand has its limits, so any surge in supply in 2025 needs to be muted, and hopefully we’ll end up with about the same number of listings as we had in 2024 – and they just come earlier.

My nine categories are full of potential home sellers, and here’s #10 – covid buyers:

Younger Americans who bought homes during the COVID-19 pandemic could account for a surprisingly large share of home sellers in the coming year, as boomers who have owned their homes for decades mostly refuse to sell, a new survey finds.

Among current homeowners, nearly 1 in 5 say they plan to sell their home next year, according to the results released on Wednesday by Bright MLS. Although people who purchased their home in the past five years accounted for just 24% of all homeowners, they made up 32% of those who plan to sell their home in 2025.

Homeowners in their 30s and 40s will be the most active group of sellers in 2025, with 27% of homeowners aged 30 to 39 and 28% of homeowners aged 40 to 49 indicating they expect to sell in the coming year. By comparison, just 10% of older homeowners plan to sell.

“Record-low mortgage rates during the pandemic were a huge incentive for individuals and families to buy a home. Many of these buyers also have been able to quickly accumulate significant equity in their homes as home prices have escalated,” says Lisa Sturtevant, Bright MLS chief economist.

In November, national median list prices were up 37% from the same month five years ago, according to Realtor.com® economic research data.

“This wealth gain has created financial security for this group of homeowners, and is also allowing them to be move-up buyers even in today’s relatively high interest rate environment,” says Sturtevant.

The Realtor.com 2025 Housing Forecast notes that the market is shifting from a strong seller’s market to one in which buyers and sellers have more balanced market power.

“As a result, sellers will need to price carefully to attract buyers, especially in markets where affordability is an issue,” says Realtor.com Chief Economist Danielle Hale.

Hale adds that while there’s potential for a favorable market for sellers, “the overall landscape will depend largely on how economic conditions, interest rates, and housing supply evolve over the first few months of the year.”

The survey found that of homeowners in their 30s and 40s who are planning to move, 30% have a mortgage with an interest rate below 4% and more than two-thirds have a rate below 5%.

Mortgage rates are currently averaging 6.69%, and the Realtor.com economic research team forecasts they will continue to average above 6% through the end of 2025.

It means that many families who plan to move will do so regardless of the higher rates. The survey found that the traditional reasons of family and career were the main impetus for moving among younger homeowners who plan to sell.

Among homeowners in their 30s who plan to sell, 37% said it would be for job reasons and 34% cited family reasons, including marriage, children, divorce, and being closer to family.

For homeowners in their 40s, the priorities were reversed, with family changes cited as the most common reason for moving, at 44%, and career changes, at 26%.

Only about 6% of homeowners aged 60-plus said they were planning to sell their home in 2025, according to the survey.

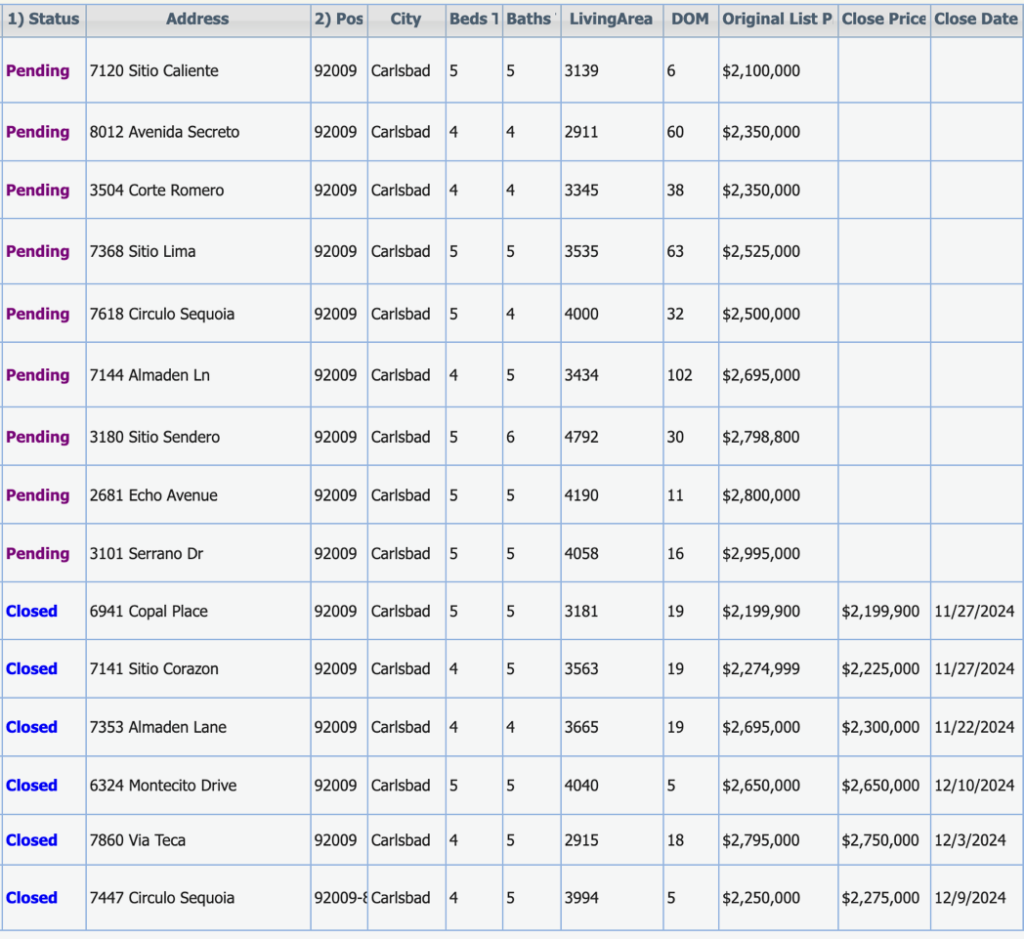

To demonstrate further how the momentum is building, let’s look at SE Carlsbad.

4th Quarter SFR Closed Sales Between $2,000,000 and $3,000,000 in the 92009:

2023: 9

2024: 23

The optimism coming off the election helped, because ALL of these went pending since November 5th:

Only one had to take a real haircut on price – so far, two sold for full price and one sold over list!

If four of the pendings close this month, it will mean that the 4Q24 sales were 3x more than last year!

True, those could have been the last buyers ever for the 92009. But doesn’t there have to be potential buyers who decided to wait-and-see what 2025 has in store? I think so, and around the 92009, there will be a strong set of recent comps to support the valuations!

It reminds me of the 4th quarter of 2012 which snuck up on us because the short sales and foreclosures had not cleared yet. The NSDCC sales in 4Q12 were 44% higher than in the previous fourth quarter, and the following year, 2013, was the hottest year of the decade.

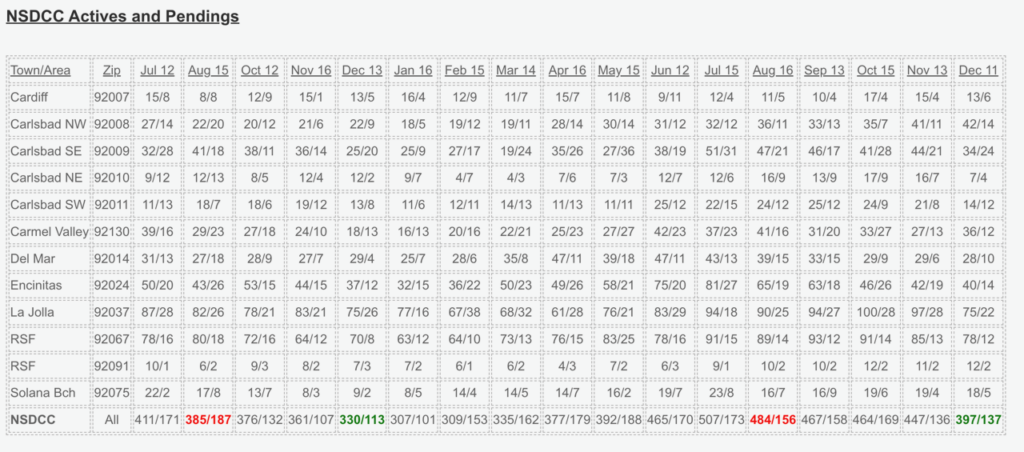

There are 20% more active listings, and 21% more pendings than we had last December – a monthly trend here in the fourth quarter of 2024 as the demand is keeping up with the supply.

Compare it to August when there were 26% more homes for sale year-over-year, but 17% fewer pendings!

The momentum going into the new year is terrific – it’s going to feel like the frenzy is back!

The holiday season is truly my favorite time of year! I love spending extra time with family and friends, decorating my home, exchanging thoughtful gifts, and taking time to reflect on the past year while dreaming up plans for the future. These traditions fill me with nostalgia, hope, and love – the perfect way to close out the year!

In the spirit of celebrating the holidays and taking advantage of this magical time, here are some San Diego events to get you feeling festive!

December 14th:

Festive 5Ks: Choose between Del Mar’s Red Nose Run along the beautiful beaches or Pacific Beach’s Santa Run in full Santa swag! Oceanside Harbor Parade of Lights: Bring a blanket, some hot chocolate and pick a comfortable spot to watch this year’s celebration. Mission Bay Parade of Lights: Kick off this holiday tradition with SeaWorld’s fireworks and a holiday boat parade on the bay.

December 15th: Pancakes & Pajamas with Santa: Visit the Pendry in downtown for a festive buffet with Santa himself. San Diego Bay Parade of Lights: A time-honored holiday tradition, the annual parade promises to dazzle and entertain bayfront crowds.

December 27th: Holiday Bowl & Parade: The scenic, bayside streets of downtown come alive with the Port of San Diego Holiday Bowl Parade (did you know it’s America’s largest balloon parade?!), followed by Syracuse vs Washington State at Snapdragon Stadium.

For the past two years, I’ve kicked off January by writing down 100 goals I want to achieve for the year ahead. Throughout the year, I cross things off, and in December, I review what I’ve accomplished, what fell through the cracks, and what’s still within reach (I’ve got 4 books left to hit my reading goal of 12 this year – wish me luck!). I love this tradition because, even though I never complete all 100 goals, I always achieve more than I expect. It’s a great way to reflect and plan for the year ahead.

The first time I did this, one of my goals was to book a tour as a professional dancer. At the time, it felt like a long shot. But come August, I landed my dream job and was on a stadium tour with Karol G – still my biggest accomplishment to date!

Whether you believe in manifestation, a higher power, or just the power of a plan, I truly believe that writing down your goals puts them into motion. So amidst the holiday fun and local events this month, why not set aside some time to dream big and write down your next great achievements? You never know what might come true!

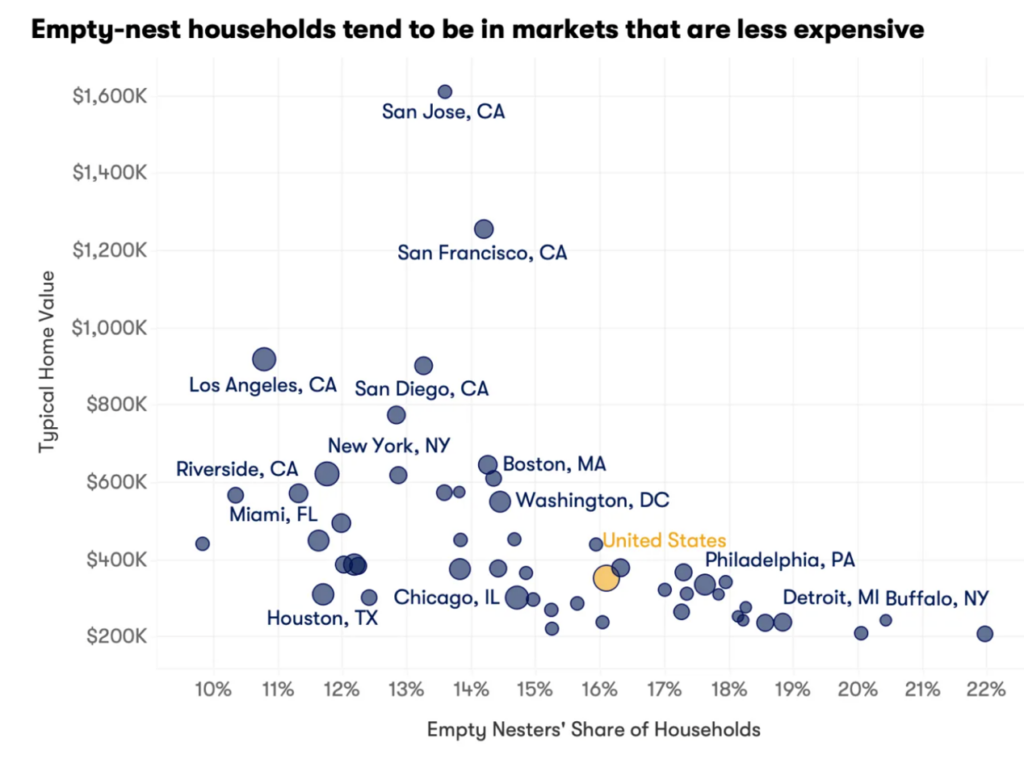

They are saying that in the expensive coastal markets there are fewer empty-nesters, but they base that opinion on the percentages? The San Diego metro of 3.3 million x 13% = 429,000 empty-nesters sounds significant to me!

Some have suggested that empty nest households – those aged 55 and older living with no children with at least two extra bedrooms and in place for at least a decade – could eventually flood the housing market with their homes and help make homes more affordable. However, data indicates that this demographic is unlikely to make a meaningful impact over the coming years, especially in the most expensive markets.

Nationwide, there were roughly 20.9 million of these empty nest households in 2022, up modestly from 20.2 million in 2017.

All else equal, in order for empty nest households to make a meaningful contribution to lowering house prices, their numbers must exceed the number of families that currently need their own housing and those that will want or need homes in the future. In addition, because relative affordability varies so widely across the country, this potential supply of homes would need to be concentrated in markets with the worst housing shortages to make a dent. Unfortunately, this future supply coming from empty-nest households doesn’t line up with the areas of greatest need on the map.

The number of empty nest households does exceed the number of families in need of housing: by 2.6 times.

There were 20.9 million empty nest households in 2022 compared to 8.1 million families living with non-relatives that were likely in need of their own unit, and that surplus has grown over time. From 2017 to 2022, the number of families doubling up — living with non-relatives — grew by 500,821. During that same period, the number of empty nest households increased by 703,892.

The problem: Most empty nest households can be found in already relatively more affordable markets. These are areas where housing is already more available, the rate of doubling up with non-relatives is much lower, and they’re located far from where the crush of current young workers choose to live.

A flood of currently owner-occupied homes hitting the market as their current owners pass away or otherwise vacate their homes will NOT solve housing affordability challenges, especially in high demand housing markets.

A silver tsunamiis likely to have a larger impact in regions like Pittsburgh and Cleveland. Younger residents have tended to leave these areas to pursue better job opportunities elsewhere, leaving older generations to make up a larger share of those who remain. Young workers choose to live near productive job centers and on the coasts, areas that have much lower populations of older retired individuals holding back housing supply in the first place.

Among the 50 largest metropolitan areas, Pittsburgh, New Orleans, Detroit, Buffalo, Cleveland were the markets with the largest gap between the potential housing supply from empty nest households and potential demand from younger residents. But these are already relatively more affordable markets with fewer home buying age workers to begin with.

In expensive coastal markets with strong job centers where home buying age workers choose to live — like Austin, Seattle and Denver — there are fewer empty nest households to begin with.

As a result, the impact of a future increase in supply coming from the existing housing stock owned by older individuals would likely have a smaller impact on affordability in expensive high demand coastal markets. Without the promise of remote work or investments that improve work prospects and raise the desirability of Midwest markets, it is unlikely that we will see a big shift in migration patterns towards markets full of empty nesters.

Rather, the fix for affordability challenges remains a strong supply expansion coming from newly built homes. Zillow research shows that housing shortages were the most severe in markets with more land use restrictions. In addition to promoting denser construction, removing barriers to homeownership that aren’t related to income — credit assistance programs, down payment assistance or help with closing costs, for example — would likely improve access to homeownership.