The big monthly jobs report is something that typically matters a great deal to rates.

Oddly enough, today’s jobs report was NOT seen having much of an impact for a few reasons. First off, analysts expected a much weaker number due to Omicron’s likely impact. Moreover, the Fed is almost exclusively focused on inflation right now as opposed to the labor market (employment and prices are the 2 key parts of the Fed’s job description). In short, no matter what today’s jobs numbers turned out to be, they weren’t likely to impact the market’s view of the Fed’s reaction.

All of that is now out the window, sort of. Although there are several important caveats regarding major seasonal adjustments, the jobs numbers were so much higher than the average forecast that markets were forced to respond. Fed rate hike expectations increased briskly and bond yields surged to their highest levels in more than 2 years.

If we disregard the once-in-a-lifetime volatility seen in March 2020 (and we absolutely should), today’s mortgage rates are now in line with the highs seen in October 2019. The average lender is now quoting conventional 30yr fixed rates in the 3.75-3.875% neighborhood. That’s a full eighth of a point higher than yesterday, and more than a full percentage point higher than the lowest rates in August 2021. Many less than perfect loan scenarios will see rates over 4%.

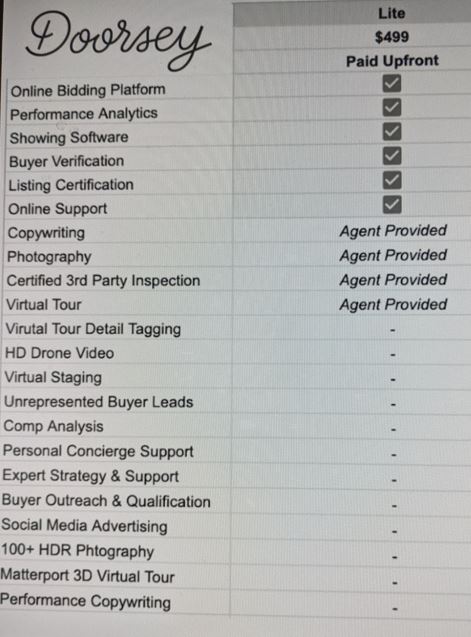

I had a good conversation this week with the people at Doorsey, and they are well on their way to providing a sharp and effective online home auction platform that could change how homes are sold. If/when Zillow buys them and provides online auctions nationwide, agents will be wondering what happened.

Doorsey, an online real estate platform founded by a group of Spokane entrepreneurs, launched this week and secured $4.1 million in a seed funding round.

Founded by Jordan Allen, Nick McLain and Matt Melville, Doorsey is an online bidding platform they say takes the guesswork out of buying a home by providing real estate agents with real-time home prices and upfront sales terms and disclosures.

“Today’s home-buying offer process is rife with frustrations for all parties,” Allen said in a statement. “Buyers and their agents want to know whether their offer can win. Sellers and their agents want to know they’re getting the best offers. And agents want to close more deals in less time.

“Doorsey solves this by allowing sellers to define upfront what it takes to win, so that buyers can compete on a level playing field and sellers can find the right buyers.”

The co-founders sought input from the local real estate community and subsequently evolved the online platform into Doorsey, which provides buyers with such things as access to home-inspection reports, sale contingencies, photos, a 3D virtual tour via Matterport and a community forum for interacting with sellers and neighbors.

Buyers can also schedule showings and view desired closing dates on the platform.

Doorsey’s listings are posted on the Spokane Multiple Listing Service and distributed through national real estate websites, including Zillow, Trulia, Redfin and Realtor.com.

Doorsey has obtained $4.1 million in seed funding – an early stage of capital investment in startups – allowing it to build-out its product, hire more employees and expand to key markets nationwide within two years, according to the company.

The funding round was led by 166 2nd Financial Services with participation from Agya Ventures, Liquid 2 Ventures and SRM Development, among other investors.

Former NFL quarterback Joe Montana is a managing partner of San Francisco-based Liquid 2 Ventures, while 166 2nd Financial Services is led by former WeWork CEO and co-founder Adam Neumann.

The South Carlsbad Coastline Project is stirring a lot of interest from people at the prospect of transforming 60 acres of city-owned land along the 101 Coast Highway. City planners held a virtual public meeting Monday to discuss the vision and hear ideas from people who live in Carlsbad.

“We really want to start with, ‘What’s the overall vision?’ We want to let people imagine what they want this space to be,” said Kristina Ray, spokesperson for the City of Carlsbad.

In May of 2020, the City of Carlsbad acquired grant funding for over $500,000 from the California State Coastal Conservancy to design a plan that would increase resilience to rising sea levels. Part of this effort would involve relocating South Carlsbad Boulevard further away from the coastline.

“We want to create more space for people, move the road over to the east a little bit, and you would free up like 60 acres worth of land,” said Ray.

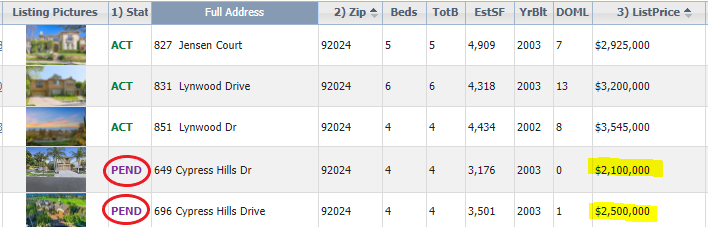

There were five new Encinitas Ranch listings that launched last week. All had open houses last weekend, and it was busy (I saw three).

It’s probably not surprising to hear that the two that went pending were the lowest-priced listings. The 3,501sf house was a one-story and on the golf course too, so their reasonable $2,500,000 list price was very attractive. The seller had talked to five Compass agents, and he told me that he wanted $4,000,000. Hopefully he got over $3,000,000?

I heard one buyer say that he was tired of the big rush in the beginning, where buyers throw crazy money at the seller. He said that he was going to hold back, and see if it happens here.

It was feeling more…..normal. Dare I say?

Darin and I are buddies so I don’t think he’d mind if we tour his listing of 649 Cypress Hills:

There will be another 20 or so new listings trickling in the coming weeks that will grow our January count. But as of today, there were only 196 houses listed for sale between La Jolla and Carlsbad last month – and 103 of them have already gone pending!

In January, 2021 we had 288 new listings.

While the 30% decline is startling, I’ll blame it on the pandemic and be optimistic about additional listings in spring making up for some of that deficit.

Last year it picked up quite a bit after January. The total count of new NSDCC listings in the first five months of 2021 was 1,780, so hopefully this year we’ll see at least 1,500 – hang in there buyers!

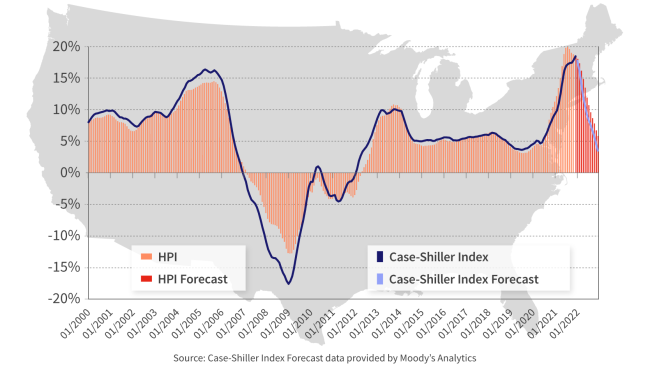

Casual observers might think this graph is saying that home prices will drop, but instead it is just the YoY change that is moderating. The MoM changes will become more interesting than the YoY changes over the next 12 months.

Home prices averaged year-over-year gains of 15 percent over the 12 months of 2021 compared to an average gain of 6.0 percent in 2020. CoreLogic’s Home Price Index (HPI) ended the year up 18.5 percent compared to the prior December. Despite indications earlier in the year that price gains were beginning to decelerate, they rose 1.3 percent in December, identical to the monthly gains reported in each of the previous three months. The annual growth is up from 18 percent in September and October.

CoreLogic says, “Consumer desire for homeownership against persistently low supply of for-sale homes created one of the hottest housing markets in decades in 2021 – and spurred record-breaking home price growth. Home price growth in 2021 started off at 10 percent in the first quarter, steadily increasing and ending the year with an increase of 18 percent for the fourth quarter.”

CoreLogic’s price forecast for this year anticipates that appreciation will exceed 10 percent for the first months of the year but will fall steadily to 3.5 percent by December 2022. The annual increases will average 9.6 percent.

The company dismisses questions about whether the nation is currently in a housing bubble. The report says its Market Risk Indicators suggest only a small probability of a nationwide price decline, pointing instead to the larger likelihood that falling prices will be limited to specific, at-risk markets. Those locations with a high probability, over 70 percent, include Prescott and Lake Havasu City-Kingman, Arizona; Merced, California; and Worcester, MA.

“Much of what we’ve seen in the run-up of home prices over the last year has been the result of a perfect storm of supply and demand pressures,” said Dr. Frank Nothaft, chief economist at CoreLogic. “As we move further into 2022, economic factors – such as new home building and a rise in mortgage rates – are in motion to help relieve some of this pressure and steadily temper the rapid home price acceleration seen in 2021.”

Prices of detached residential properties posted an annual increase of 19.7 percent in December. This was 5.5 percent higher than the appreciation of attached properties at 14.2 percent.

The state with the greatest increase continues to be Arizona at 28.4 percent, It is followed by Florida at 27.1 percent and Utah at 25.2 percent. Two Florida cities, Naples, and Punta Gorda, posted the largest gains among metro areas at 37.6 and 35.7 percent, respectively.

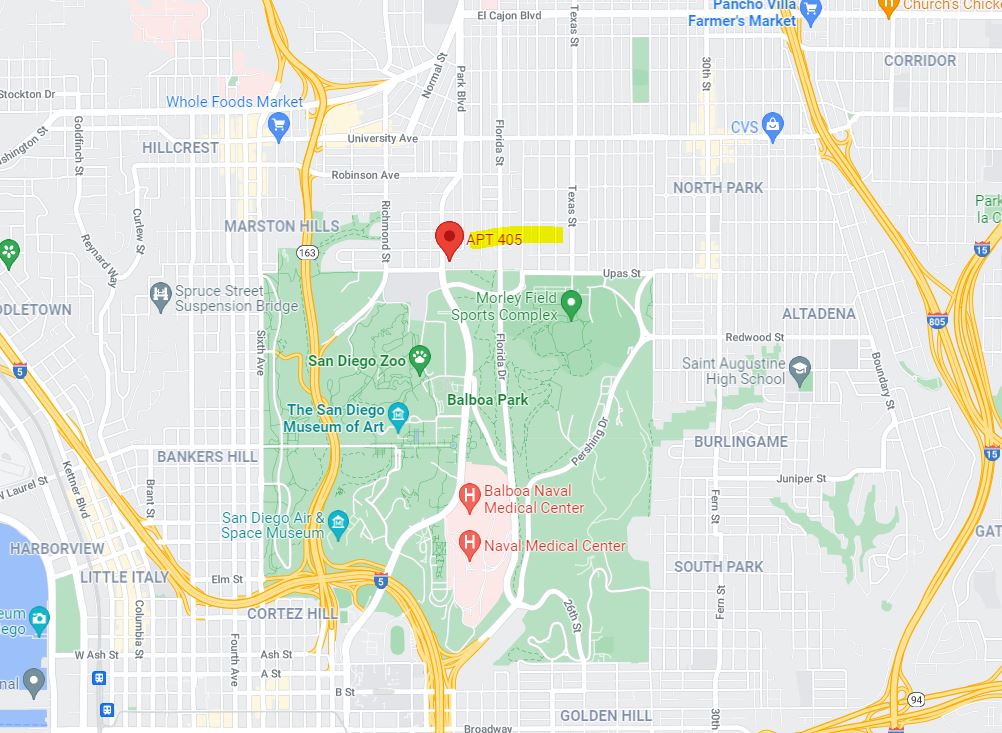

Check out our new listing of this 2br/2ba home in Park Royal! It’s the premium penthouse unit in the complex, located in the very back and has the wrap-around balcony for max viewing of the surrounding area. Newer kitchen, newer bathrooms, hardwood floors, efficient mini-splits, and plenty of natural light. Want move-in ready? This is it – just bring your toothbrush! Two pets allowed too! Balboa Park is a treasure – live right next to it! Morley Field is a block away, which has cycling, dog park, swimming, tennis, golf (27 holes) archery, softball, frisbee golf….everything you need to enjoy the outdoors! Only $695,000.

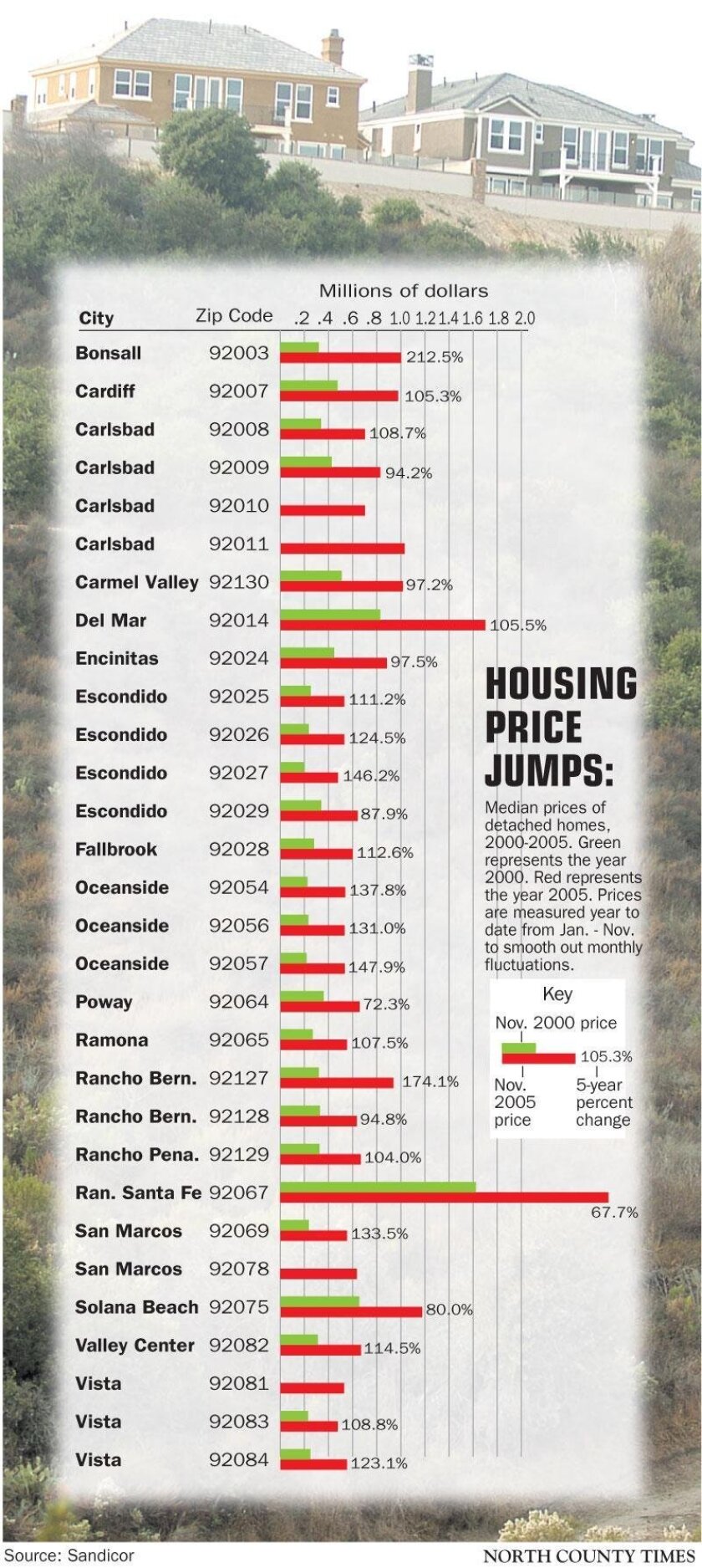

Has there ever been a precedent to our current housing frenzy? Yes – back in the 2000-2005 era, which a new blogging guy coined, ‘The Golden Age of Real Estate’ (bubbleinfo.com was three months old). Note the S&P Index:

Date: December 25, 2005

The median price of a single-family home in North County, and in California as a whole, has roughly doubled in the last five years. That familiar statistic implies that virtually anyone who bought in 2000 and sold five years later reaped a profit.

California and the rest of the U.S. benefited from low interest rates, enabling people to buy more expensive homes than they otherwise would have been able to afford, said Jim Klinge, a Carlsbad-based Realtor.

And in San Diego County, price increases of about 20 percent a year became expected, encouraging people to buy at any cost, in the expectation of sure profits.

By comparison, other investments didn’t look so good in the aftermath of the collapse of the stock market bubble, which began in 2000. For example, the Standard & Poors index of 500 stocks closed on Nov 1, 2000, at 1,429.40. As of Nov. 1, 2005, the S&P500 closed at 1,202.76. (today it’s at 4,480).

The real estate increases fueled spending by homeowners, who got ready cash from their rising home equity. A strong economy, with lower unemployment than the state and national averages, helped people buy, turning the county into one of the hottest real estate markets in America.

That market cooled down this year, with most months posting only single-digit gains over the same month in 2004. (November, with a 14 percent year-over-year increase in North County single-home median prices, was an exception.)

Real estate professionals have said the slowdown was inevitable since prices, along with factors such as the ratio of monthly mortgage payments to rental payments, have gotten far out of whack. A study by Torto Wheaton Research this year found that San Diego County’s rental-to-buy payment ratio was 40 percent, the lowest of any of the major markets it studied.

“I think we’ll look on these last five years as the golden age of real estate,” Klinge said. “The increases in the median price, both locally and countywide, have been astonishing for Realtors and buyers and sellers alike. We won’t see this again for the foreseeable future.”

But the gains weren’t evenly distributed. Depending on where the home is located, that potential profit varies from marginal —— in percentage terms, but not necessarily in dollars —— to outstanding.

As 2006 is about to begin, Klinge said prospective buyers should think long term. With prices as high as they are, the potential for quick gains that lured “flippers” to buy houses only to sell them a short while later is nearly gone.

With more sellers on the market, the buy-at-all-costs mentality of a short while ago has vanished, Klinge said. Homes will still sell, but at a slower rate and a lower price. Sellers can’t count on big profits, and prices could even fall at times, he said.

“I would say the market is going to be completely driven by buyers buying a house to live in,” Klinge said. “So if you’re going to buy a house, make sure it’s going to last you for years.”

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.