This topic came up in my 45 hours of continuing education, and Donna agreed that rarely do listing agents comment on their seller’s disclosures – do they even read them? A focal point as we transition into single agency:

To complete the disclosure process, the seller’s agent filters property information provided by the seller before it is provided to the prospective buyer.

Accordingly, all property information received from the seller is reviewed by the seller’s agent for inaccuracies or untruthful statements known or suspected to exist by the seller’s agent. Corrections or contrary statements by the seller’s agent necessary to set the information straight are entered on the disclosure forms before the information is used to market the property and induce prospective buyers to purchase, collectively referred to as fair and honest dealings.

The extent to which disclosures about the physical condition of the property are to be made is best demonstrated by what the seller’s agent is not obligated to provide. Everything else adversely affecting value and known to the seller’s agent – material facts – are to be brought to the attention of prospective buyers as a matter of law.

As a minimum effort to be made before handing a prospective buyer information received from the seller, the seller’s agent is to:

review the information received from the seller;

include comments about the agent’s actual knowledge and observations made during their visual inspection of the property which expose the inaccuracies or omissions in the seller’s statements; and

identify the source of the information as the seller.

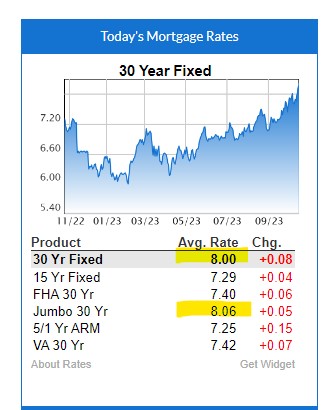

People might think that 8% mortgage rates will kill the real estate market, but they are one more thing that can be fixed with money.

Two popular strategies to lower the mortgage rate:

30-year fixed rate buydown: Paying one point, or 1% of the loan amount will lower the rate by 1/4%. It would take a few points paid to make a significant difference, and the home seller can contribute too. On a $2,000,000 purchase with 25% down and a loan amount of $1,500,000, the monthly payment is $11,006 at the 8% rate. But the payment can be permanently reduced to $9,358 per month (6.375%) by paying six points, for a savings of $1,648 per month! Hopefully the seller will contribute some or all of the fee.

2-1 temporary rate buydown: Paying 2.4 points will lower the mortgage rate by 2% in the first year, and then by 1% in the second year. With the same $1,500,000 loan, here’s how the 2-1 buydown looks:

In both of those examples, you have a fixed-rate 30-year mortgage. If you are more of a gambler and don’t want to pay any points, the other alternative is to get the 3/1 ARM that has a fixed rate of 6.25% for three years, and then the rate adjusts annually for the remaining 27 years.

Or you can buy a Toll Brothers home:

A side note on Toll Brothers. Their Del Mar Mesa tract where construction was getting underway? They did sell all of those homes.

The number of former Californians who became Texans dropped slightly last year, but some of that slack was picked up by Arizona and Florida, which saw their tallies of ex-Californians grow, according to new state-to-state migration figures released Thursday.

The flow of Californians to Texas has marked the largest state-to-state movement in the U.S. for the past two years, but it decreased from more than 107,000 people in 2021 to more than 102,000 residents in 2022, as real estate in Texas’ largest cities has grown more expensive. In Florida, meanwhile, the number of former Californians went from more than 37,000 people in 2021 to more than 50,000 people in 2022, and in Arizona, it went from more than 69,000 people to 74,000 people during that same time period.

California had a net loss of more than 113,000 residents last year, a number that would have been much higher if not for people moving to the state from other countries and a natural increase from more births than deaths. More than 343,000 people left California for another state last year, the highest number of any U.S. state.

Housing costs are driving decisions to move out of California, which with 39 million residents is the most populous U.S. state, according to Manuel Pastor, a professor of sociology and American Studies & Ethnicity at the University of Southern California.

“We are losing younger folks, and I think we will see people continuing to migrate where housing costs are lower,” Pastor said. “There are good jobs in California, but housing is incredibly expensive. It hurts young families, and it hurts immigrant families.”

Natalie’s last show with Karol G was in Boston and because it could be the last show ever, we felt compelled as committed parents and fans to attend. This was my first trip to Boston and because many of my best friends were born and raised there, and because it was Natalie’s birthday, we had to tour Fenway:

In 2019, the state legislature passed a bill that had two profound impacts:

It prohibits an owner of residential real property from terminating a tenancy without just cause.

It also prohibits an owner of residential real property from, over the course of any 12-month period, increasing the gross rental rate for a dwelling or unit more than 5% plus the percentage change in the cost of living, as defined, or 10%, whichever is lower, of the lowest gross rental rate charged for the immediately preceding 12 months, subject to specified conditions.

As you probably suspected from the title, these are more of the tenant-friendly laws that prevail in California! If this is the last straw and you’re ready to sell your rental property, contact me today!

Currently, every listing agent is required to offer some sort of buyer-agent compensation on the MLS. Zillow and Redfin publish those commission amounts on every listing now, so they are all out in the open.

Today, there are 79 homes for sale between La Jolla and Carlsbad in the $2,000,000-$3,000,000 price range. Thirty percent of those listing agents are offering less than 2.5% commissions to the buyer-agents.

Outsiders who see that will assume that commissions are finally starting to drop, after all these years.

But the vast majority of those listing agents are probably still taking 5% to 6% commissions, and offering 2% or less to the buyer-agent (and more for themselves).

If the listing agent is supremely talented and brings special skills to the transaction, then it would be understandable. But I’ve been a buyer-agent on listings that are offering less than 2.5%, and they’re not different. Virtually every listing agent still practices the Three-P marketing plan: Put a sign out front, Put it in the MLS, and Pray.

There are hundreds of multiple listing services in America. So far, only a few have removed the requirement of offering a buyer-agent commission. But the NAR lawsuits are going to change that, and soon every MLS will permit 0% commissions to be offered to the buyer-agents (hoping buyers will pay their own agent).

The listing agents who have little or no repsect for the buyer-agents will keep offering them lower and lower commissions. Eventually, their rate will get down to zero or close.

Will sellers figure it out?

Sellers focus on the total commission. They don’t do enough transactions to know that the amount the listing agent pays to the buyer-agent will impact the sale. It is a bounty offered to encourage the sale of the house, and when market conditions are soggy, it is better to pay buyer-agents more commission, not less.

In the lawsuits, they will discuss agents steering their buyers to homes that pay higher commissions. It’s why the search portals publish the commission rates now so buyers can track whether their agent shows any bias based on the commission rate being offered.

It’s why the industry will be racing towards 0% commissions offered to the buyer-agents.

Eventually, the DOJ will probably step in and insist that ALL sellers pay 0% commission to the buyer-agents to insure there is no chance of steering. Instead, listing agents will just offer them spiffs under the table in a softer market or when the house is ‘unique’.

Until then, the listing-agent teams are going to keep offering lower and lower commissions (if any) to the buyer-agents – who will then try to get their buyers to pay them something….anything!

At the same time, the listing agents will be encouraging buyers to avoid paying a buyer-agent commission altogether by coming direct to the listing agent instead. Their in-house assistant-agents will attempt a faux representation of the buyer but it will just be a novice clerk who processes their paperwork.

Boom! The seller didn’t have to pay a buyer-agent commission – making these lawsuits worth it – and instead the listing agent keeps the whole commission. If buyer-agents can somehow wedge themselves into the deal, then great, but will the buyer pay them too, when it doesn’t seem necessary?

Mark my words – this will be standard fare in the next year or two.

Morgan Stanley analysts previously expected national home prices to fall 4% in 2023, as the housing market continued to crater, and reaffirmed their pessimistic forecast in April of this year. But the analysts recently changed their tune in a big way: They now say housing prices could rise up to 5% for the year.

The reversal, made in a research note earlier this week, comes as mortgage rates continue to rise, hitting 8%, the highest level since 2000. The increase has had a profound impact on the housing market, but not necessarily as many people had expected.

For one thing, it’s keeping the supply of homes for sale tight largely due to the lock-in effect, which prevents homeowners that have lower mortgage rates from selling because it would require buying a new home at a much higher interest rate. That’s helping to prop up the market by creating big demand for the relatively few houses for sale, further deteriorating affordability.

Morgan Stanley isn’t the only financial institution to suggest home prices will likely increase. Roger Ashworth, a managing director at Goldman Sachs, recently wrote that despite affordability being worse than in the 2008 housing crash, housing itself is in a much stronger position, largely due to a low supply of homes for sale.

“Absent any negative shocks to the broader economy that would either boost excess supply of homes on the market or fuel an uptick in unemployment, we continue to expect home prices to rise at a slow pace,” he wrote. And he predicts that by the end of this year, home prices will rise 1.8%, with a 3.5% increase by the end of 2024.

People are asking about the NAR lawsuits – hat tip to Susie, Gerry, and Carl!

The lawsuit that began this week contends that realtors force sellers to pay a commission to the buyer’s agent. Two defendants, ReMax and Anywhere (Coldwell Banker, Sotheby’s, etc.) have already come to settlement agreements, though they haven’t been approved by the judge yet. The other two brokerages, Keller Williams and Berkshire Hathaway, plus the National Association of Realtors are the remaining defendants. Their attorney started the proceedings by declaring that the plaintiffs have the burden of proof, and the defense may not call a witness. It is that type of arrogance that got them into this mess!

A summary:

In their trial brief, the plaintiffs in the suit allege that NAR’s Participation Rule, which they refer to as the Mandatory Offer of Compensation Rule, is “a market-shaping and distorting rule” that stifles innovation and competition.

“The Rule requires every home seller to offer payment to the broker representing their adversary, the buyer, even though the buyer’s broker is retained by and owes a fiduciary obligation to the buyer (who may be told, falsely, that the services of the buyer broker are “free”),” the brief said.

They argue that the current practice of the seller’s agent splitting their commission with the buyer’s agent, who typically negotiates for a lower selling price for their client, works against the seller’s interest and only exists due to the alleged anticompetitive rules. The plaintiffs also note that the NAR rule in question requires a blanket offer of compensation for the buyer’s broker regardless of their experience or the level of service they provide the buyers with, and that the compensation offer was only visible to the buyer’s agent and not their clients, until very recently.

“This artificial and severed market structure created by Defendants’ conduct deters price-cutting competition and innovation, resulting in inflated commissions,” the brief states. “The Mandatory NAR Rules impede the ability of a free market to function in the residential real estate industry, and the plain purpose and/or effect of the Rules is to raise, inflate, or stabilize commission rates.”

In the brief, the plaintiffs claim that the other defendants in the suit colluded with NAR to enforce this and other NAR and MLS policies.

“The Corporate Defendants compel compliance in multiple ways, including by requiring their franchisees, subsidiaries, brokers, and agents become members of NAR; writing the NAR Rules into their own corporate documents; and requiring that their franchisees, subsidiaries, brokers, and agents become members of and participants in the Subject MLSs — entities that compel NAR membership and adopt the mandatory NAR Rules,” the brief reads.

The brief notes that Craig Schulman, the director of Berkeley Research Group and professor of economic data analytics at Texas A&M University, will be an expert witness for the plaintiffs at trial. In studying transaction data from NAR and other parties, the brief states the Schulman has concluded that “(a) the NAR Rules have anticompetitive effects; (b) the NAR Rules caused a seller to pay his adversary (buyer broker) and that, but for the conspiracy, a seller would not pay the buyer broker; and (c) all class members were impacted.”

The brief also notes that Schulman will testify that NAR’s rules have stabilized commission rates at an “anticompetitive level,” noting that commissions have remained at 6% for several years.

Unfortunately, none of the reality of what happens on the street will get introduced during the trial. Instead, it will be ivory-tower guys hoping to persuade the judge and jury (one of which has to breast-feed her infant every 1.5 hours) that the whole commission thing is out of control and someone is to blame.

But the defendants have a good point:

NAR also argued that the plaintiffs do not have the ability to sue for damages —which some believe could reach as much as $4 billion in this case — because under federal and Missouri antitrust law, only “direct purchasers” can be allowed to sue and the plaintiffs have not bought anything directly from NAR or the other defendants.

“And, according to those same Model Rules and listing agreements, Plaintiffs did not directly pay cooperating agents, NAR, or the other Defendants; sellers only directly pay their listing agents and only directly receive services from their own agents,” the brief states. “Therefore, at best, Plaintiffs might claim that they paid their listing agents (who are not parties to this case) who, only then, paid Defendants. But such an indirect claim is prohibited by Supreme Court case law.”

Home sellers pay the full commission to the listing brokerage. It is the listing agent who declares in the original listing agreement of how much of the full commission they are willing to pay the buyer’s agent. None of this will be discussed during this trial, but it’s the most important part!

The plaintiffs should be suing the individual listing agents – good luck with that!

In the end, the defendants might be found guilty, and they will appeal for years – the American way! Or it’s more likely that they will settle in the next couple of weeks because the ReMax and Anywhere settlements were only $55 million and $85 million, which is pennies.

Part of the settlement package will be that the MLS will no longer be obligated to display ANY commission to be paid to the buyer’s agent. It will cause two things to happen:

MORE steering by the buyer-agents to the homes that are paying a healthy commission (bounty).

Buyer-agents trying to convince their buyers to pay them the buyer-side commission.

Kayla is faced with this dilemma in New York City. Did you know that 2/3’s of the population in Manhattan are renters? It’s a big business! But the listing agents don’t offer a tenant-agent commission, which means Kayla has to get paid by her tenants upon finding them new home to rent.

The results:

She has had the landlord’s listing agent pull aside her potential tenant and tell her to ditch Kayla and save the money, and go through him directly. Apparently they aren’t concerned with their reputations!

She has also had her potential tenants be reluctant to sign an tenant-agent agreement because they see apartments being advertised by the listing agents. They want to reserve the right to go direct to the listing agent, and usually they do. As a result, Kayla only works with those who appreciate her advice.

The idea that home buyers will hire and pay their own buyer-agents is a great idea…..in theory.

The reality is that buyers will go direct to the listing agents when they see an interesting new home for sale. Those listing agents will be advertising to those buyers directly, and flat-out encourage them to get a better deal by going through them.

Doug Duncan, chief economist at Fannie Mae, was acknowledged as the best forecaster in America last year when he was honored with the Lawrence R. Klein Award for Blue Chip Forecast Accuracy, one of the best-known and longest-standing achievements in economic forecasting.

The winner is selected based on the accuracy of forecasts published in the Blue Chip Economic Indicators newsletter, compiled and edited by Haver Analytics, Inc. “It is a real honor for the Fannie Mae forecast team to be recognized with the Lawrence R. Klein Award,” said Duncan.

“The award is based on the smallest average error for GDP, CPI, and unemployment over the past four years,” says Professor of Economics Dennis Hoffman, director of the Office of the University Economist at ASU. “I commend Doug Duncan and his team at Fannie Mae for their remarkable predictions during a period of extensive market fluctuation and instability.”

Trustindex verifies that the original source of the review is Google.

We sold a home with Jim and Donna and from beginning to end they were consummate professionals. Their initial walk through the property resulted in a list of items to be repaired or updated. They supplied a list of vendors and job quotes to do the repairs and updates. We originally wanted to sell ‘as is’ and just get it over with. They gave us a selling price for ‘as is’ and options for doing a few updates/repairs to doing it all with the selling price for each option. We agreed to do all they suggested and we sold for the exact price they predicted. For every dollar spent we got back more than $2 back in the selling price. And they got that price in a rising interest rate environment! Donna and Jim are extremely detailed and guide you through ever aspect of the sale. There were no surprises thanks to their guidance. We couldn’t be more pleased with their representation.

Thank you Donna and Jim,

Jerry and Mary

Heather Quejada

March 27, 2025

Trustindex verifies that the original source of the review is Google.

We have known Jim & Donna Klinge for over a dozen years, having met them in Carlsbad where our children went to the same school. As long time North County residents, it was a no- brainer for us to have the Klinges be our eyes and ears for San Diego real estate in general and North County in particular. As my military career caused our family to move all over the country and overseas to Asia, Europe and the Pacific, we trusted Jim and Donna to help keep our house in Carlsbad rented with reliable and respectful tenants for over 10 years.

Naturally, when the time came to sell our beloved Carlsbad home to pursue a rural lifestyle in retirement out of California, we could think of no better team to represent us than Jim and Donna. They immediately went to work to update our house built in 2004 to current-day standards and trends — in 2 short months they transformed it into a literal modern-day masterpiece. We trusted their judgement implicitly and followed 100% of their recommended changes. When our house finally came on the market, there was a blizzard of serious interest, we had multiple offers by the third day and it sold in just 5 days after a frenzied bidding war for 20% above our asking price! The investment we made in upgrades recommended by Jim and Donna yielded a 4-fold return, in the process setting a new high water mark for a house sold in our community.

In our view, there are no better real estate professionals in all of San Diego than Jim and Donna Klinge. Buying or selling, you must run and beg Jim and Donna Klinge to represent you! Our family will never forget Jim, Donna, and their whole team at Compass — we are forever grateful to them.

Lou F

March 27, 2025

Trustindex verifies that the original source of the review is Google.

WeI had the pleasure of working with Klinge Realty Group to sell our home in Carmel Valley, and I cannot recommend them highly enough!

Jim and Donna demonstrated exceptional professionalism, offering expert guidance on market conditions and pricing strategy, which resulted in a quick and successful sale.

Communication was prompt and we were well-informed throughout the entire process.

For anyone looking for a dedicated and knowledgeable real estate team, look no further!

---

William Sams

March 25, 2025

Trustindex verifies that the original source of the review is Google.

Donna and Jim Klinge of Klinge Realty Group have our highest possible recommendation. From Donna and Jim’s first visit to our house through closing their advice and counsel was candid and honest in all dealings. They kept us fully informed throughout the process. The house sold less than three days after listing with a two-week closing. My wife and I have sold several houses during our lives. This was by far the best experience. Klinge Reality is a premium service realtor. You can’t make a better choice for someone to sell your home fast and for top dollar.

Emily Hernandez

December 29, 2024

Trustindex verifies that the original source of the review is Google.

Donna and Jim provided exceptional support and professionalism throughout the entire process. We couldn't have been happier with their efforts. They made our house shine, and thanks to their expertise, it sold above the listing price in the very first weekend! Truly a fantastic experience from start to finish.

Jesus Adrian Sahagun

November 11, 2024

Trustindex verifies that the original source of the review is Google.

This year has been difficult on our family, mainly due to having to sell our home. Thankfully we knew God had a plan for us and working with the Klinge team was a key part of it. It was an obvious decision to work with them again after such an amazing experience when purchasing the same home we needed to sell. The challenge was, how will we do this in so little time with so much going on? Jim and Donna held our hand every step of the way. Whenever an unexpected issue arose they found and provided a solution. Never once did we feel pressured to make a decision and the Klinges were always reassuring after providing the information that the decision was ours to make. Despite the curve balls, they never panicked and exemplified the “can do” attitude, making us feel optimistic and taken care of. Their expertise and professionalism was superb. But of all the reasons to work with the Klinges, the most impactful and valuable is their compassion and genuine care for their clients. We pray that we can one day purchase our forever home and you better believe that Jim and Donna will be representing us - as long as they will have us of course. Thank you again Klinge team! Your execution, experience, and care are unmatched.

SABIHA PASHA

July 23, 2024

Trustindex verifies that the original source of the review is Google.

Jim and Donna were fantastic! Jim understanding my needs, recommending potential places, pointing out the pros and cons of each property was invaluable. Then when the offer was accepted Donna’s organized guidance through the inspections, paperwork etc made the whole process seem effortless.

So grateful that I had them on my side!

Anu Koberg

July 13, 2024

Trustindex verifies that the original source of the review is Google.

We first found Jim through his blog at bubbleinfo.com, which really showcased his knowledge of SoCal real estate. Since then we've done three transactions with Jim and Donna, and they are an incredible full service agency, with Jim's deep market insight and Donna's deft contract and project management. We trust them implicitly in their analysis and strategy, which is based on years of experience. They're always available and on top of things, and we strongly recommend them to anyone.

Bjorn Isachsen

July 10, 2024

Trustindex verifies that the original source of the review is Google.

The Good

The Klinge Realty Group operates like a finely tuned machine, with a very personal touch. We contacted them on a Sunday and they were talking to us about our family and our needs on our living room couch the following day. They carefully listened to us and worked with us to identify the best and quickest path to listing within 2 weeks to take advantage of the low inventory conditions in our South Carlsbad neighborhood. They knew our tract specifically and had many previous sales there over the years - they came prepared with a thorough analysis of comparative sales and recommended a pricing strategy that they felt confident would yield offers the first weekend on the market.

The Great

Over the next two weeks Donna coordinated a range of vendors who she knew from experience could get the preparation to list work we needed done on time and with high quality. Our light tune-up involved excellent experiences with their stagers, landscapers, contractors, electricians, and plumbers. Throughout this period Donna's daily communication was clear, concise, and responsive. Any time we had questions Donna picked up the phone or texted immediately - but almost always, she answered our questions before we even knew we had them.

The Outstanding

We had a tricky situation with a shared fence that could have delayed our escrow. Donna used superb mediation skills to negotiate the terms of replacement and was personally on site with the fence contractor to make sure everything went smoothly. The fence looks great and escrow closed on time.

The Truly Exceptional

Our house came on the market on a Wednesday and between then and Monday morning Jim was personally at all three open houses. He was in constant communication explaining potential buyer reaction and strength. As he predicted offers began to come in on Saturday and each one was incrementally higher than the last. At the end we had 5 offers, 4 of which were over list, and the final accepted offer was $100,000 over list. In addition to being over list it included rent back terms that met our needs.

The Recommendation

For all of these reasons we would strongly recommend The Klinge Team to anyone wanting to sell in North County Coastal San Diego. I had been reading Jim's bubbleinfo.com blog for 15 years and knew when the time came to sell that he would be our first call. Jim Klinge is not your standard realtor. He is keenly aware of market conditions and sales strategies. And, works his tail off - though not as hard as Donna . At this point he's gone from realtor to friend and I plan to have him over to grill and chill at our new place to talk real estate, but also just about life and raising kids in San Diego. He's more interested in relationships than his sales numbers - and that's why his sales numbers are so high. We have already recommended the Klinge's to some close friends and another successful sale is on deck right around the corner...

Chris Shea

June 21, 2024

Trustindex verifies that the original source of the review is Google.

We recently had the pleasure of working with Jim and Donna from Klinge Realty Group to sell our house, and we couldn't be more satisfied with the experience. From the initial meeting, they listened attentively to our needs and provided invaluable guidance on specific improvements to get our home market ready.

Their responsiveness throughout the entire process was truly impressive. Anytime we had questions or concerns, they were quick to address them, ensuring we felt comfortable and informed every step of the way. What stood out the most was their team and extensive network of tradespeople, which made addressing any necessary repairs or updates seamless and stress-free.

Thanks to their expertise and dedication, our house sold quickly and at a great price. We highly recommend Jim and Donna to anyone looking to buy or sell a home. They are a fantastic team who truly care about their clients and deliver exceptional results.